Income Tax Act Section 40

Will Salaried Class Be Happy From India S 2019 Budget Quora Budgeting Paying Taxes Standard Deduction

143 1 Notice From Income Tax How To Reply For Notice Under Section 143 1 Section 143 1 Reply Youtube Income Tax Income Income Tax Return

Format Of Partnership Deed As Per Income Tax Act Partnership Deed Taxact Income Tax Custom Writing

Section 87a Tax Rebate Fy 2019 20 How To Check If You Are Eligible For The Tax Rebate How To Check If You Are Eligible To Claim Sect Wealth Tax Rebates Tax

Income Tax Slabs In Pakistan 2016 17 Income Tax Rates For Salaried Persons Http Ift Tt 29rpbo5 Income Tax Tax Rate Income

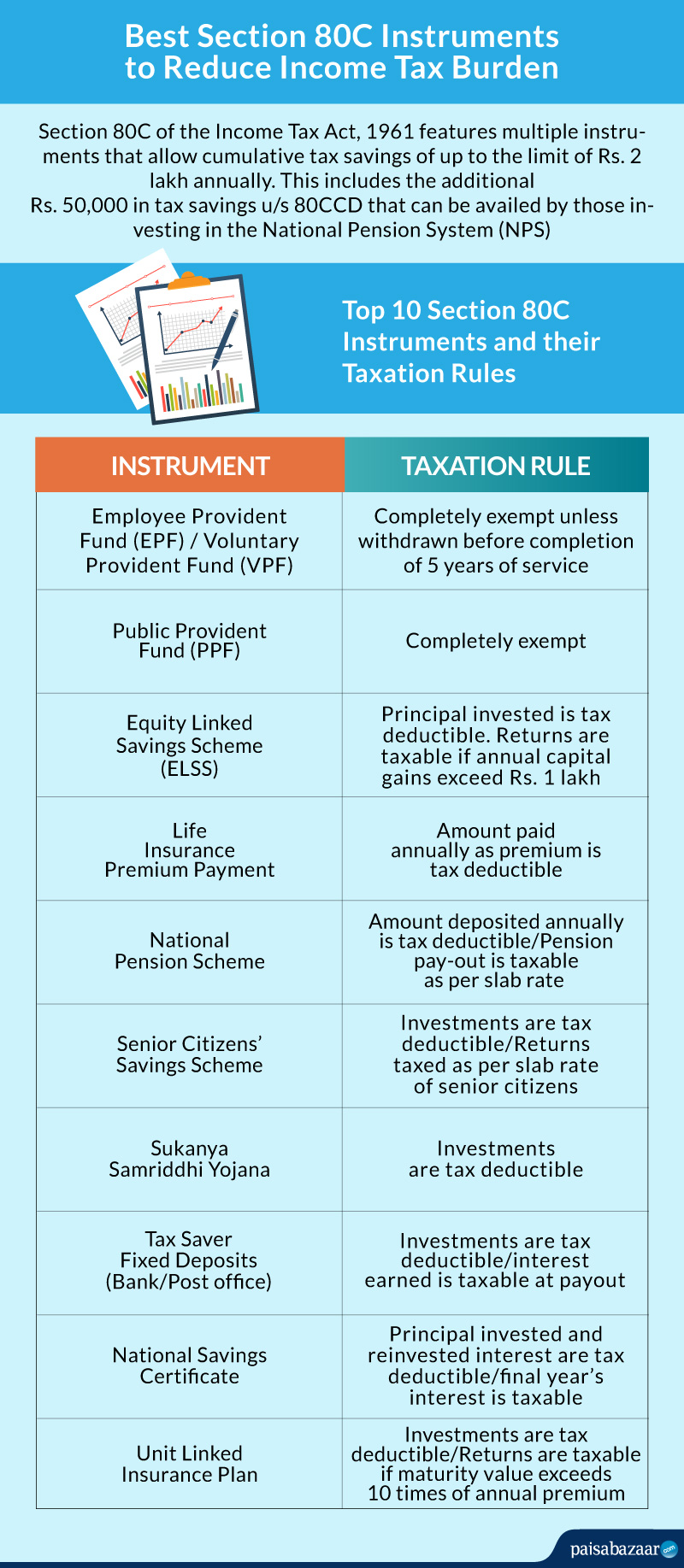

Section 80c Deduction Under Section 80c In India Paisabazaar Com

40 1 except as otherwise expressly provided in this part.

Income tax act section 40. Inserted by the income tax amendment act 1972 w. However there is certain restriction on such deduction of expenses. Where the assessee incurs any expenditure in respect of which payment has been made or is to be made to certain specified persons i e.

Section 40 in the income tax act 1995. A in the case of any assessee. Certain expenses cannot be allowed as deduction.

Relatives or close associates of the assessee and the assessing officer is of the opinion that such expenditure is excessive or unreasonable having regard to the fair market value of the goods services or facilities for which the payment is made or the. Section 40 of income tax act 1961 2017 amounts not deductible. Section 40 a v in the income tax act 1995.

Chapter iv sections 14 59 of income tax act 1961 deals with provisions related to computation of total income. V 2 1. Section 40 b of income tax act places some restrictions and conditions on the deductions of expenses available to an assessee assessable as a partnership firm in relation to the remuneration and interest payable to the partners of such firm.

A a taxpayer s gain for a taxation year from the disposition of any property is the amount if any by which. An entity identified in column 3 of an item in the table as not holding a depreciating asset cannot hold the asset under. 1 short title 2 part i income tax 2 division a liability for tax 3 division b computation of income 3 basic rules 5 subdivision a income or loss from an office or employment 5 basic rules 6 inclusions 8 deductions 9 subdivision b income or loss from a business or property 9 basic rules 12 inclusions.

That means it had overriding effect on section 30 to 38. Section 40 40a of the income tax act 1961 specified it. Notwithstanding anything to the contrary in sections 30 to 38 the following amounts shall not be deducted in computing the income chargeable under the head profits and gains of business or profession.

This Is Why Filing Your Income Tax Return Will Never Be The Same Income Tax Return Income Tax Federal Income Tax

Pin On Full Forms

60 40 Asset Allocation Provides Best Returns Over A Period Article Writing Personal Finance Finance

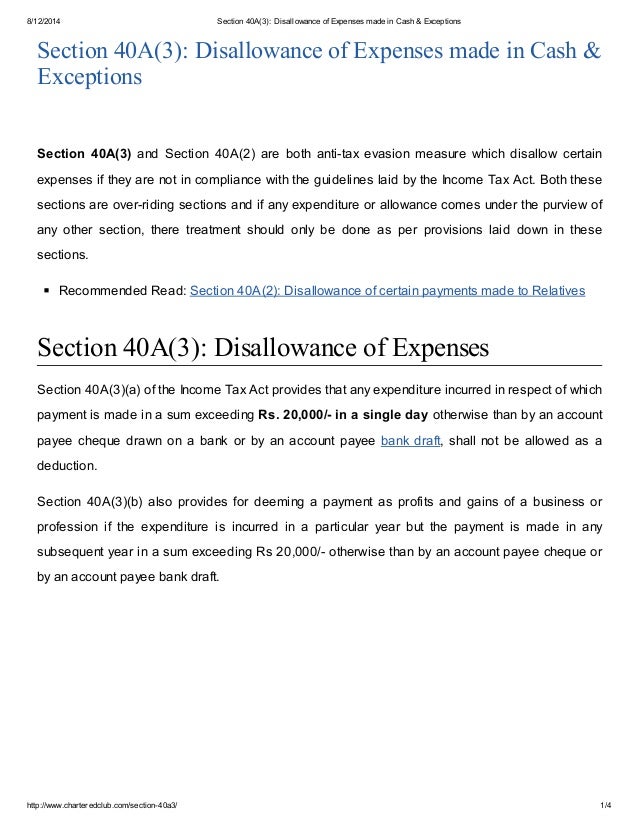

Section 40 A 3 Disallowance Of Expenses Made In Cash Exceptions

Managerial Remuneration Under The Companies Act 2013 Managerial Persons Covered Taxation Acting Management Central Government

40a Ia Non Deduction Of Tds 30 Disallowance Deduction Income Tax Income

Income Tax Form W5 Five Precautions You Must Take Before Attending Income Tax Form W5 In 2020 Tax Forms W4 Tax Form Form

Pin By Karthik Shetty On India General Knowledge Facts Legal Advice Income Tax Preparation

Accounting Taxation Income Tax Slab Rates For A Y 2015 16 And 2016 17 Applicability Of Surcharge And Education Cess Income Tax Income Tax

America S High Corporate Income Tax Rate Harms Global Competitiveness Mercatus Center Income Tax Tax Rate Income

E Filing Home Page Income Tax Department Government Of India Income Tax Income Government

Understanding Your Form 16 Income Tax Return Income Tax Filing Taxes

Old Or New Tax Slabs For Fy 2020 21 Amount At Which Tax Are Same Incometax Budget Unionbudget2020 Oldvsnew In 2020 Indirect Tax Income Tax Tax