Income Tax Act Section 85

This Is Why Filing Your Income Tax Return Will Never Be The Same Income Tax Return Income Tax Federal Income Tax

Pin About Goods And Service Tax On Taxguru

Https Moj Gov Jm Sites Default Files Laws The 20income 20tax 20act 0 Pdf

Rationalization With Section 43ca Of The Income Tax Act 1961 Under The Existing Provisions Contained In Section 50c In Case Of Tr Taxact Capital Assets Case

Residential Status Under Income Tax Act 1961 Revisited

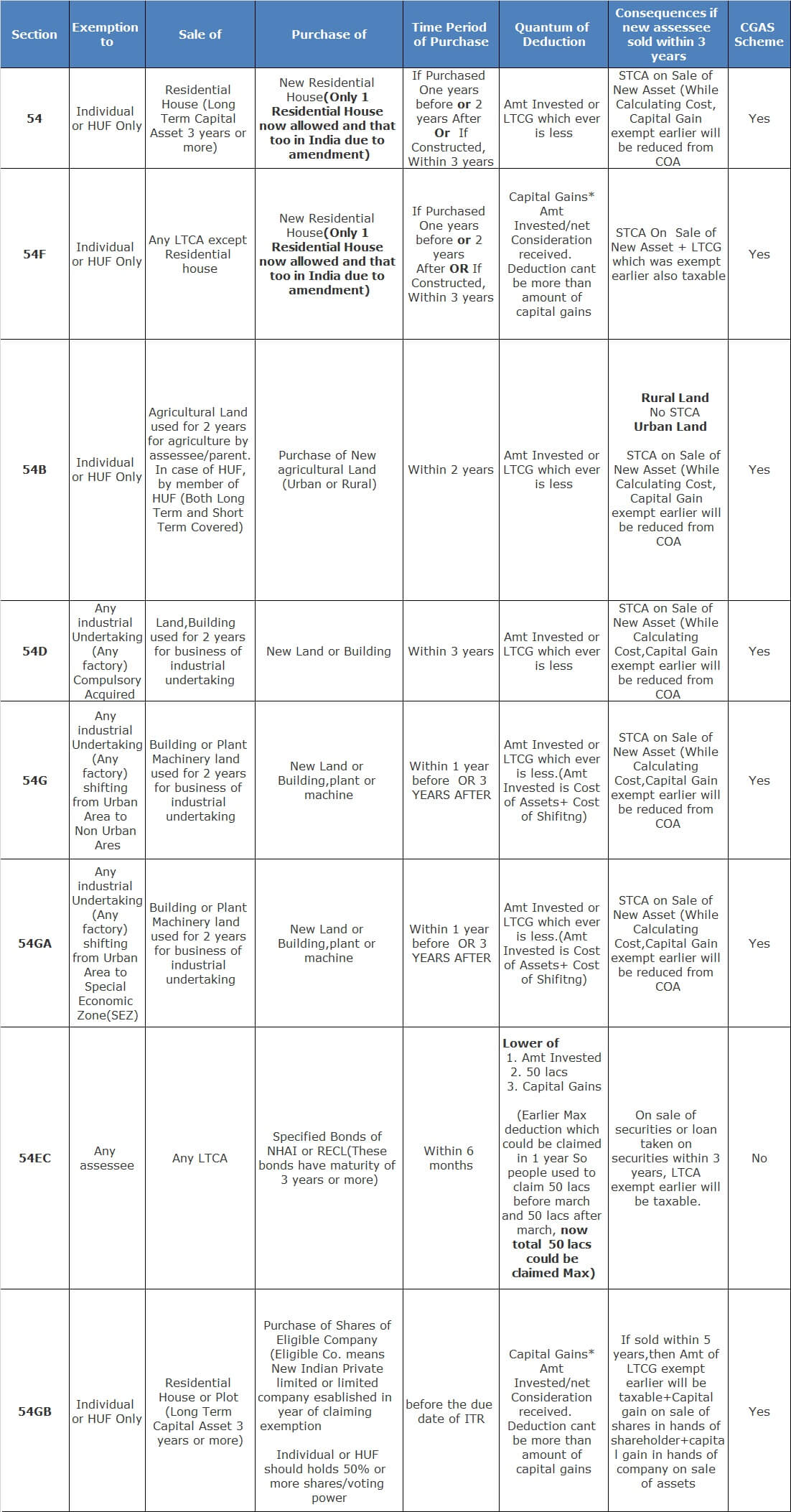

Section 54 Income Tax Act Capital Gains Exemption Chart Teachoo

Through section 85 of the income tax act certain types of eligible property can be transferred to a transferee corporation.

Income tax act section 85. 2 1 where subsection 85 1 or 85 2 applies to a disposition of property other than a disposition of property to which section 84 1 or 212 1 applies to a corporation by a person or partnership in this. The income tax act ita contains several provisions that allow a taxpayer to transfer ownership of property without any immediate tax consequences with section 85 being one such provision. The general rule is that transfers of property take place at fair market value fmv and consequently any money made on a sale over what was paid for the property is known as a capital gain and taxes must be paid on that amount.

85 02 have been changed to the tourism development act ch. 1 short title 2 part i income tax 2 division a liability for tax 3 division b computation of income 3 basic rules 5 subdivision a income or loss from an office or employment 5 basic rules 6 inclusions 8 deductions 9 subdivision b income or loss from a business or property 9 basic rules 12 inclusions. Section 40 of the tourism development act preserves.

In other words it allows a taxpayer to defer paying taxes on assets transferred. Note on hotel development act 2000 all references in the income tax act to the hotel development act formerly ch. 85 1 1 where shares of any particular class of the capital stock of a canadian corporation in this section referred to as the purchaser are issued to a taxpayer in this section referred to as the vendor by the purchaser in exchange for a capital property of the vendor that is shares of any particular class of the capital stock in this section referred to as the exchanged shares.

This is especially useful for sole proprietorships looking to incorporate or for transfers between affiliate companies. Paragraphs 85 1 a to 85 1 i are applicable with such modifications as the circumstances require in respect of the disposition as if the partnership were a taxpayer resident in canada who had disposed of the property to the corporation. Subsection 85 1 permits a taxpayer and subsection 85 2 permits all members of a partnership to elect to defer all or part of the income which would otherwise arise on the transfer of certain types of property to a taxable canadian corporation.

Section 85 permits eligible transferors to elect jointly with a transferee corporation on the transfer of property to fix an agreed amount which both parties use to account for the transfer for income tax purposes. The transfer is often called a rollover because it can take place at the cost of the property thereby avoiding the immediate recognition of accrued gains. A section 85 tax rollover rollover is term used to describe a special tax technique that allows a taxpayer to defer all or part of the income which would otherwise be taxed upon transfer.

Eligible property can include capital property canadian and foreign resource properties some types of inventory and some types of real estate. Section 85 of the income tax act the act allows you to transfer property to a canadian corporation without immediate tax consequences.

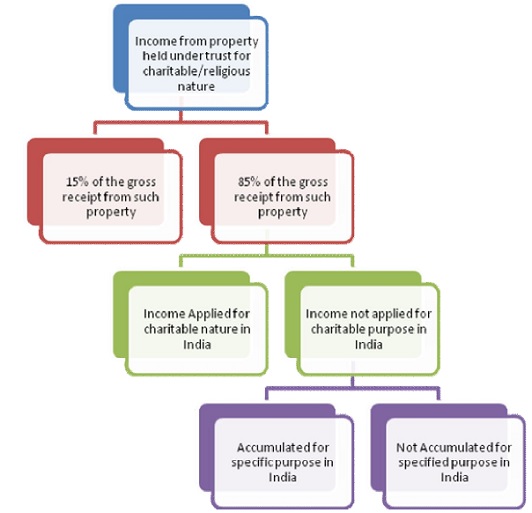

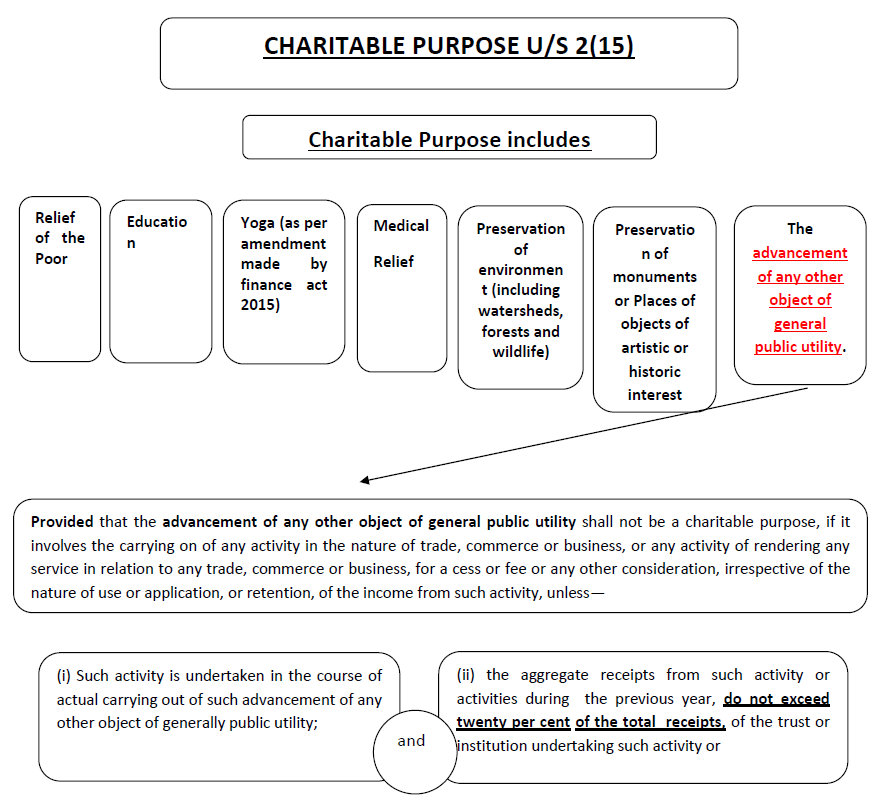

Taxation Of Charitable Religious Trust

Canada Tax Developments In Response To Covid 19 Kpmg Global

Provisions Of Charitable Trust As Amended By Finance Act 2020

Health Insurance Provides You With A Security For You And Your Family During Medical Emergencies Acc Health Insurance Policies Income Tax Buy Health Insurance

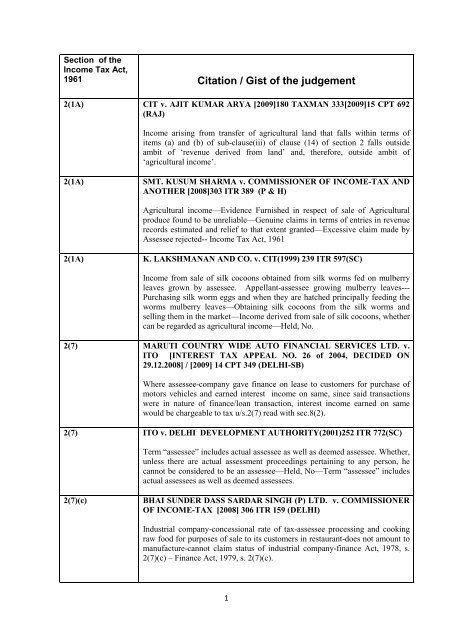

Citation Gist Of The Judgement Nadt

2018 Tax Calculator Calculate Your Estimated Taxes Finance Tips Finance Tips Income Tax Calculator

Want To Buy A Plot Of Land Here S A Lowdown On Things You Must Know Stuff To Buy Smart Money You Must

Master Guide To Income Tax Act 1961 With Images Income Tax Taxact Income

Bombay High Court Sets Aside Cbdt Action Plan Of Rewarding Cits Frases Celebres

Business News Live Share Market News Read Latest Finance News Ipo Mutual Funds News Business News Finance Marketing

Beware Of The Government Reconciling Your Income Disclosed In The Income Tax Return With Your Expenditure On Jewellery Luxurycars W Income Tax Incom

Section 54f Amended Benefit Of Capital Gain Will Be Available To One Property Only In 2020 Capital Gain Taxact Income Tax

Important Definitions Inthe Income Tax Act Ppt Video Online Download