Internal Revenue Code Section 125

Https Www Scgov Net Home Showdocument Id 35454

New Irs Guidance Provides Employers With Section 125 Plan Flexibility During 2020

Ssa Poms Si 00820 102 Cafeteria Benefit Plans 07 23 2012

Celebrating 40 Years Of Section 125 Cafeteria Plans Core Documents

2019 Section 125 Plan Document Updates Core Documents

Irs Section 125core Documents

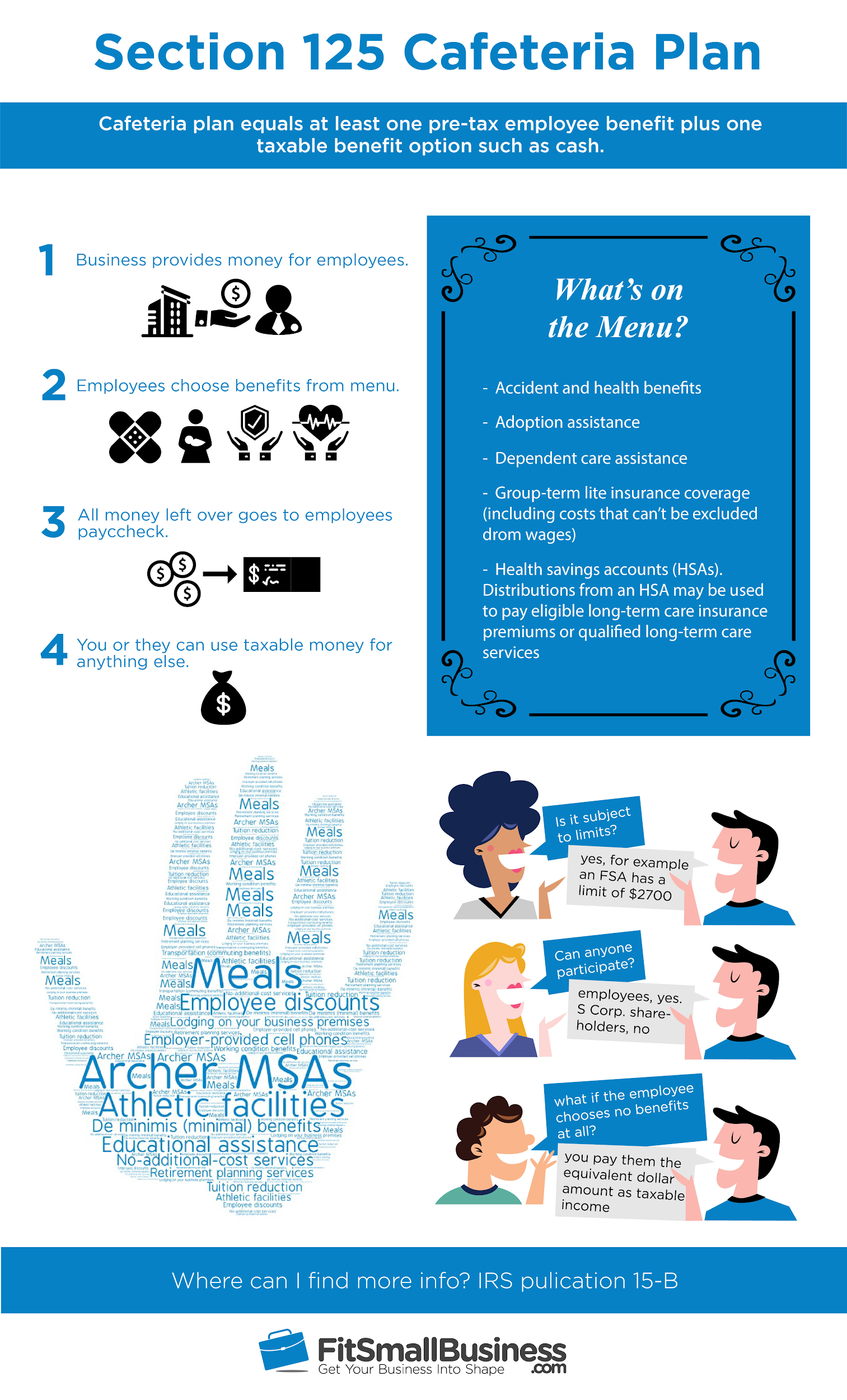

For a complete understanding of the rules see the proposed regulations under code section 125.

Internal revenue code section 125. For provision that for purposes of section 125 of the internal revenue code of 1986 a plan shall not be treated as failing to be a cafeteria plan solely because under the plan a participant elected before january 1 1988 to receive reimbursement under the plan for dependent care assistance for periods after december 31 1987 and such. With the rules of internal revenue code code section 125 and related internal revenue service irs regulations. Under these rules a section 125 plan must have a written plan document and can only offer certain qualified benefits on a tax favored basis.

While self employed individuals may maintain a section 125 plan for their employees only. Section 125 f defines a qualified benefit as any benefit which with the application of 125 a is not includable in the gross income of the employee by reason of an express provision of chapter i of the internal revenue code other than 106 b 117 127 or l32. Some of the.

For provision that for purposes of section 125 of the internal revenue code of 1986 a plan shall not be treated as failing to be a cafeteria plan solely because under the plan a participant elected before january 1 1988 to receive reimbursement under the plan for dependent care assistance for periods after december 31 1987 and such. The above discussion provides only the most basic rules governing a cafeteria plan. Section 125 of the internal revenue code refers to cafeteria plan benefits.

Maximize Your Tax Savings From Your Section 125 Plan American Fidelity

Http Doa Alaska Gov Drb Pdf Employer Cafeteriaplans Slidesnoteshandout Pdf

Section 125 Covid 19 Relief Irs On 2020 Mid Year Elections Fsa Claims Core Documents

Cafeteria Plan Section 125 Features Costs Providers

Covid 19 Relief For Section 125 Plans And Increase In Fsa Carryover

What Is A Section 125 Pop Premium Only Plan Gusto

Is Your Section 125 Plan Compliant American Fidelity

5 Things Districts Need To Know About Section 125 Cafeteria Plans

Https Www Dms Myflorida Com Content Download 140605 907025 Cafeteria Plan 2018 Pdf

Cafeteria Plan Options For 2020 Section 125 Pop Hsa Fsa Dcap Core Documents

Understanding Section 125 Cafeteria Plans

Taxation Of Irs Section 125 And Health Insurance Finance Zacks

Client Alert Irs Relaxes Section 125 Mid Year Change Rules Increases Health Fsa Carryovers Fraser Trebilcock Jdsupra