Internal Revenue Code Section 152

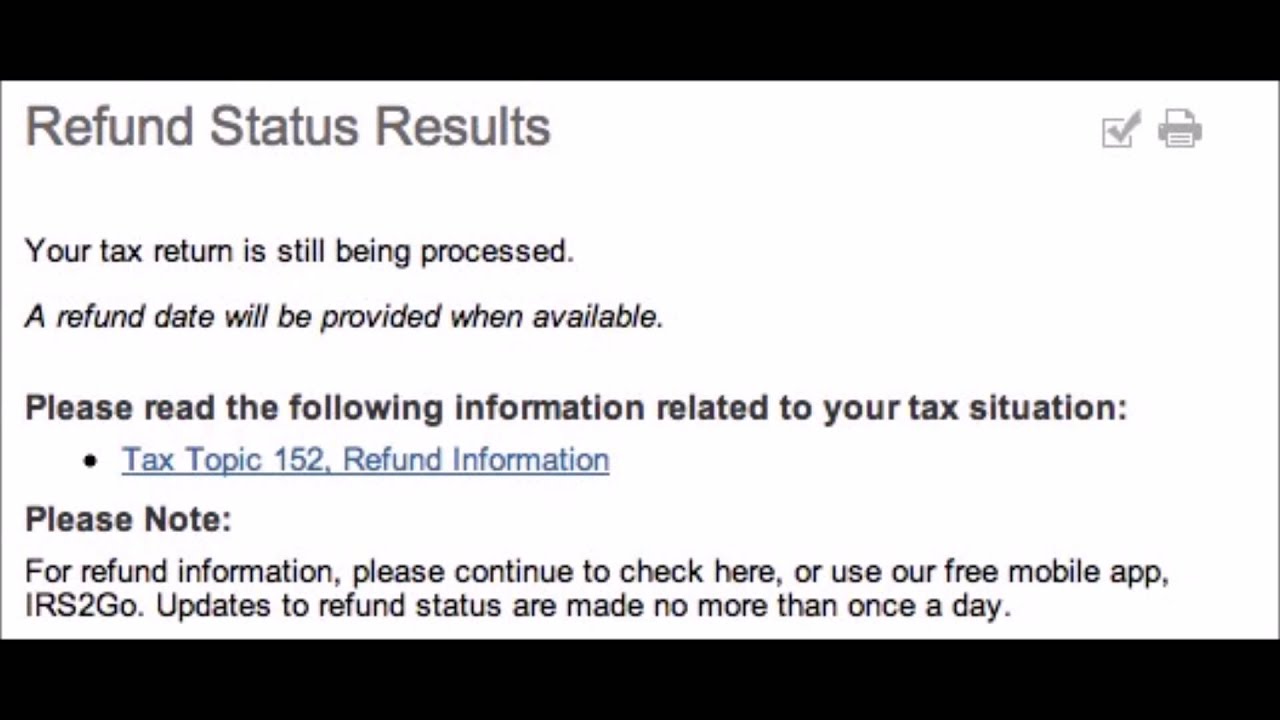

Irs Reference Codes On Where S My Refund Refundtalk Com

A Research Example Tax Research Federal Guides At Georgetown Law Library

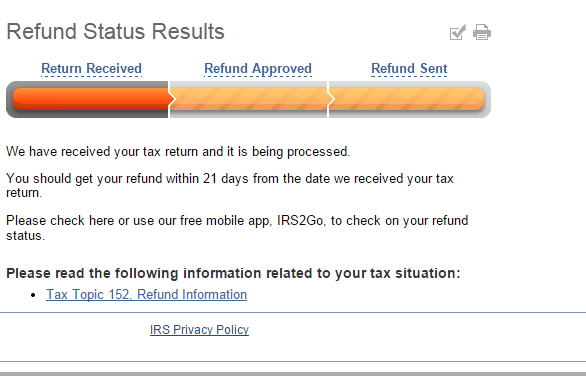

On The Irs Check My Refund Website It Says Tax Topic 152 Now After I Went Through A Very Gruesome Audit That Lasted Over A Year It Used To Say Tax Topic

Tax Implications And Rewards Of Grandparents Taking Care Of Grandchildren The Cpa Journal

3 12 37 Imf General Instructions Internal Revenue Service

Refund Schedule Posts Facebook

/GettyImages-57173091-66f9b5d085fc4aa780d30dc7d2261489.jpg)

Internal revenue code 152.

Internal revenue code section 152. 85 866 applicable to taxable years beginning after dec. Location in internal revenue code title 26 internal revenue code subtitle a income taxes chapter 1 normal taxes and surtaxes subchapter b computation of taxable income part v deductions for personal exemptions statute sec. 152 b 2 married dependents an individual shall not be treated as a dependent of a taxpayer under subsection a if such individual has made a joint return with the individual s spouse under section 6013 for the taxable year beginning in the calendar year in which the taxable year of the taxpayer begins.

Dependent defined on westlaw findlaw codes are provided courtesy of thomson reuters westlaw the industry leading online legal research system. 31 1953 and ending after aug. This notice provides guidance under section 152 d of the internal revenue code for determining whether an individual is a qualifying relative for whom the taxpayer may claim a dependency exemption deduction under section 151 c.

Section 152 d 1 d provides that an individual is not a qualifying relative of the taxpayer if the. 85 866 set out as a note under section 165 of this title. Amendment by section 4 a c of pub.

16 1954 see section 1 c 1 of pub. For purposes of this section 1 dependents ineligible.

Who Does The Irs Consider To Be A Qualifying Relative Accountingweb

3 12 179 Individual Master File Imf Unpostable Resolution Internal Revenue Service

Sec 163 Interest

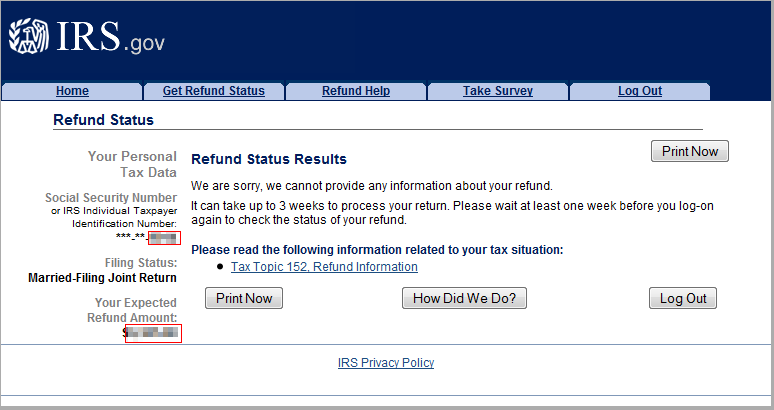

Refund Status Refundtalk Com

Https Cao 94612 S3 Amazonaws Com Documents Deferred Comp Withdrawal Form Covid Related V2 Pdf

Https Www Yu Edu Sites Default Files Inline Files Irsdefinitionsection152 0 Pdf

Why Do Where S My Refund Bars Disappear Youtube

Https Hr Umich Edu Sites Default Files Declaration Tax Status Oqa Pdf

We Cannot Provide Any Information About Your Refund Refundtalk Com

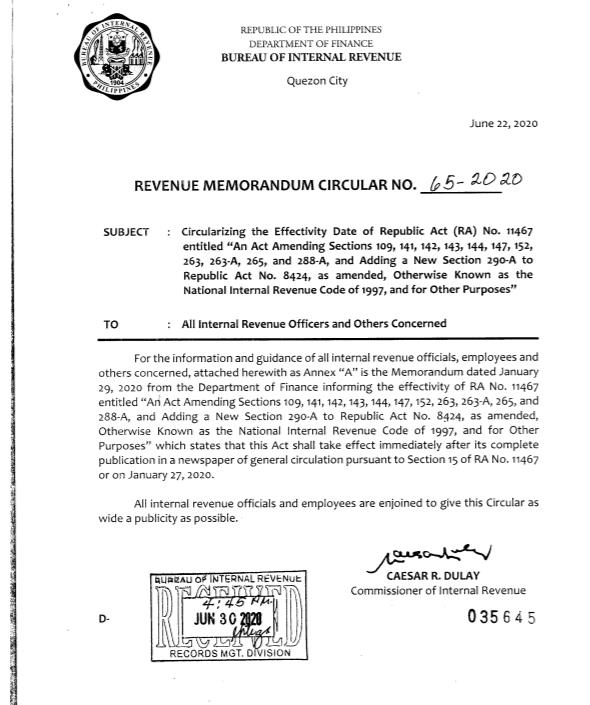

Ra No 11467 S Effectivity Date Is January 27 2020 Grant Thornton

Internal Revenue Code Irc

Federal Register Updated Disclosure Requirements And Summary Prospectus For Variable Annuity And Variable Life Insurance Contracts

Why Is It Taking So Long To Get My Tax Refund And Why Your 2020 Refund May Be Delayed By The Irs Aving To Invest