Internal Revenue Code Section 61

Article What Are Some Common Tax Myths Link Inside Gain Followers Argument Irs

Complete Internal Revenue Code Winter 2021 Edition Law Firms Tax Thomson Reuters

W 12 Form Online 12 Mind Blowing Reasons Why W 12 Form Online Is Using This Technique For Ex Tax Forms Irs Forms Fillable Forms

32 1 1 Overview Of The Regulations Process Internal Revenue Service

Internal Revenue Bulletin 2020 29 Internal Revenue Service

3 12 10 Revenue Receipts Internal Revenue Service

Neither the statute nor the regulations define the term transactions.

Internal revenue code section 61. 2095 provided that no regulations be issued in final form on or after oct. 1954 ceased to have effect on the day after nov. Chapter 1 normal taxes and surtaxes.

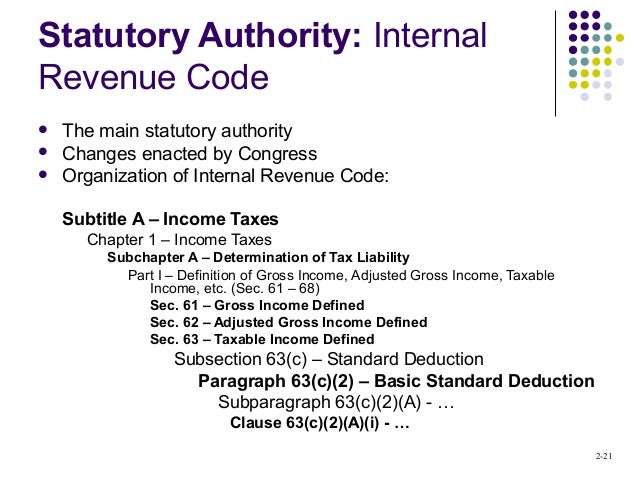

Section 61 of the internal revenue code provides that gross income means all income from whatever source derived. 8 1978 pursuant to section 210 a of that act. Subtitle a income taxes.

See below for the section as effective for divorce or separation instruments executed after dec. 1 1977 and before july 1 1978 providing for inclusion of any fringe benefit in gross income by reason of section 61 of the internal revenue code of 1986 formerly i r c. The united states supreme court has interpreted this to mean that congress intended to express its full power to tax incomes to the extent that such taxation is permitted under arti.

Internal revenue code 61. 3097 as amended by pub. Part i definition of gross income adjusted gross income taxable income etc.

22 1986 100 stat. 8 1978 92 stat. Findlaw codes are provided courtesy of thomson reuters westlaw the industry leading online legal research system.

8 1978 92 stat. 22 1986 100 stat. 31 2018 a general definition.

Instructions For Form 5471 02 2020 Internal Revenue Service

Non Foreign Affidavit Under Irc 1445 Legal Forms Internal Revenue Code Real

Tax Refund Tax Services Tax Refund Business Tax

Student Loan Tax Deduction Simplified With Images Tax Deductions Student Loans Student Loan Interest

These Are The Most Important Numbers On Your Tax Return Federal Income Tax Tax Return Paying Taxes

Understanding Income Taxes Visual Ly Income Tax Tax Organization Tax Prep

4 19 10 Examination General Overview Internal Revenue Service

Acct321 Chapter 02

The Complete Internal Revenue Code Summer Edition Law Firms Tax Thomson Reuters

Internal Revenue Bulletin 2020 15 Internal Revenue Service

Internal Revenue Bulletin 2017 26 Internal Revenue Service

Aca Compliance Bulletin Final Form For Aca Reporting Sterlingrisk Insurance Bulletin Compliance Report

Account Suspended Where Are You Now Navy Veteran Looking For Someone