Irc Section 119

Vince Nardone Tax And Controversy Irs Concludes Free Employee Meals Are Not Excludable Under Irc Section 119

Issues With A President S House On Campus Association For Biblical Higher Education

Blog Viewer Net Assets

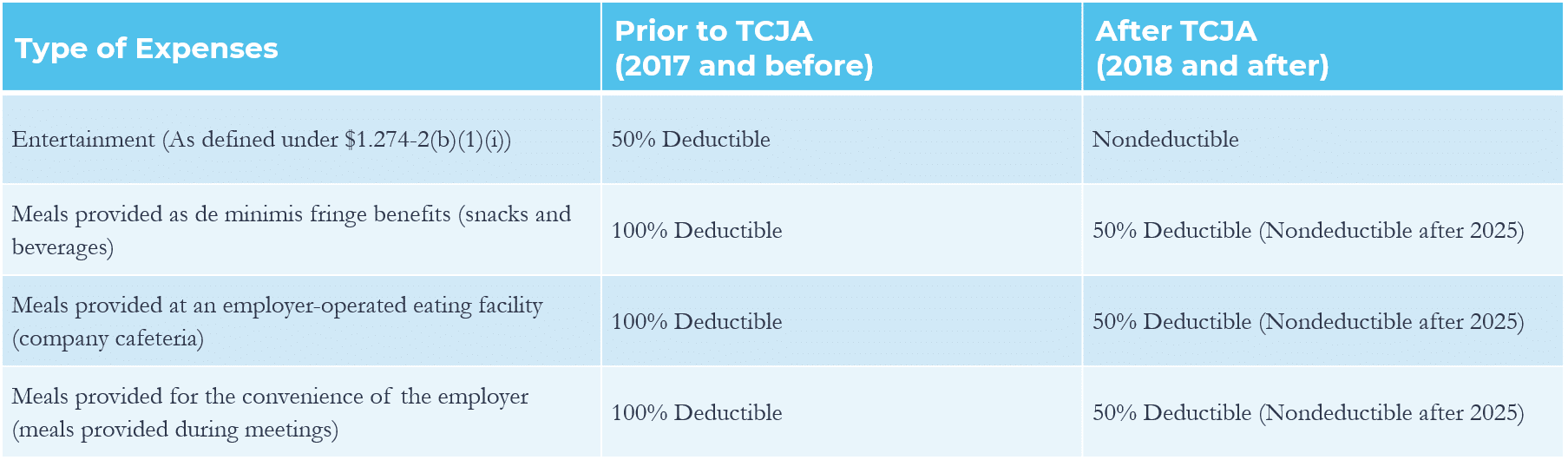

Navigating The New Meals And Entertainment Deductions Under Tcja Grf Cpas Advisors

Employer Provided Lodging Expenses Castro Co

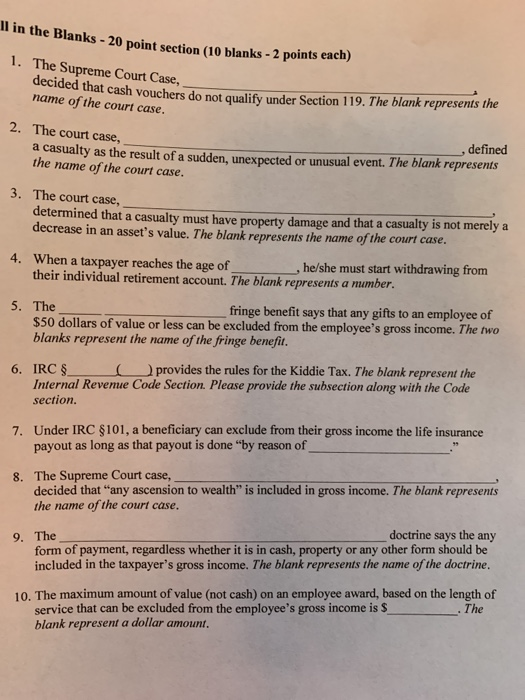

Solved Il In The Blanks 20 Point Section 10 Blanks 2 Chegg Com

Computation of taxable income.

Irc section 119. Since the enactment of section 119 however courts have tended to apply section 119 by resorting to pre section 119 concepts. At other times taxpayers have successfully used section 119 complying with its. 119 u s.

119 a meals and lodging furnished to employee his spouse and his dependents pursuant to employment there shall be excluded from gross income of an employee the value of any meals or lodging furnished to him his spouse or any of his dependents by or on behalf of his employer for the convenience of the employer but only if. The exclusion provided by section 119 applies only to meals and lodging furnished in kind by or on behalf of an employer to his employee. Some courts have strained to apply section 119 to partic ular fact situations when it seemed fair to do so.

Code unannotated title 26. A meals and lodging furnished to employee his spouse and his dependents pursuant to employment. Execute full text search of the most current edition of 26 c f r.

Items specifically excluded from gross income. There shall be excluded from gross income of an employee the value of any meals or lodging furnished to him his spouse or any of his dependents by or on behalf of his employer for the convenience of the employer but only if 1 in the case of meals the meals are furnished on the. Meals or lodging furnished for the convenience of the employer.

Go after clicking through the exit link below enter your search terms and then click the search button. Meals or lodging furnished for the convenience of the employer. Internal revenue code section 119 a meals or lodging furnished for the convenience of the employer.

Section 119 a 2 of the code provides that there shall be excluded from the gross income of an employee the value of any lodging furnished to the employee the employee s spouse or any of the employee s dependents by or on behalf of the. If the employee has an option to receive additional compensation in lieu of meals or lodging in kind the value of such meals and lodging is not excludable from gross income under section 119. Exclusively designed by section 119.

3 12 23 Excise Tax Returns Internal Revenue Service

The Exclusion For Meals And Lodging

Https Treatedwood Com Assets Uploads Documents Products D Blazeirc R302 Fire Resistant Pdf

Irs Attempts To Tighten Rules For Business Meal Exclusions Lexology

Substance Not Form Determines Whether Employee Meals Have Noncompensatory Business Reason Irs Warns Ogletree Deakins

Fringe Benefits Affected By The Tax Cuts And Jobs Act Ogletree Deakins

Employer Provided Meals Recent Irs Guidance Provides A Cautionary Tale Sc H Group

Tax Cuts And Jobs Act Effect On Meals And Entertainment Dermody Burke Brown

W 119d Fill Online Printable Fillable Blank Pdffiller

On Premises Meals Is There Such A Thing As A Free Lunch

Final Report

Pretest Probability Cornerstone Of Testing In Suspected Ischemic Heart Disease Circulation Cardiovascular Imaging

2013 2020 Form Ny Dtf St 119 2 I Fill Online Printable Fillable Blank Pdffiller