Irc Section 162 E

Pin On Mourning Gun Violence

Pin By Kristy Sims On Words Of Wisdom With Images Breakup Healing A Broken Heart Broken Heart

Tools To Live By One Minute Ultrasound Ultrasound Ultrasound Tech Diagnostic Medical Sonography

The Edge Of The World Beachy Head Is A Chalk Headland On The South Coast Of England Close To The Town Of East White Cliffs Of Dover Beautiful Places Scenery

Cash Accounting Method Unlocked Dallas Business Income Tax Services

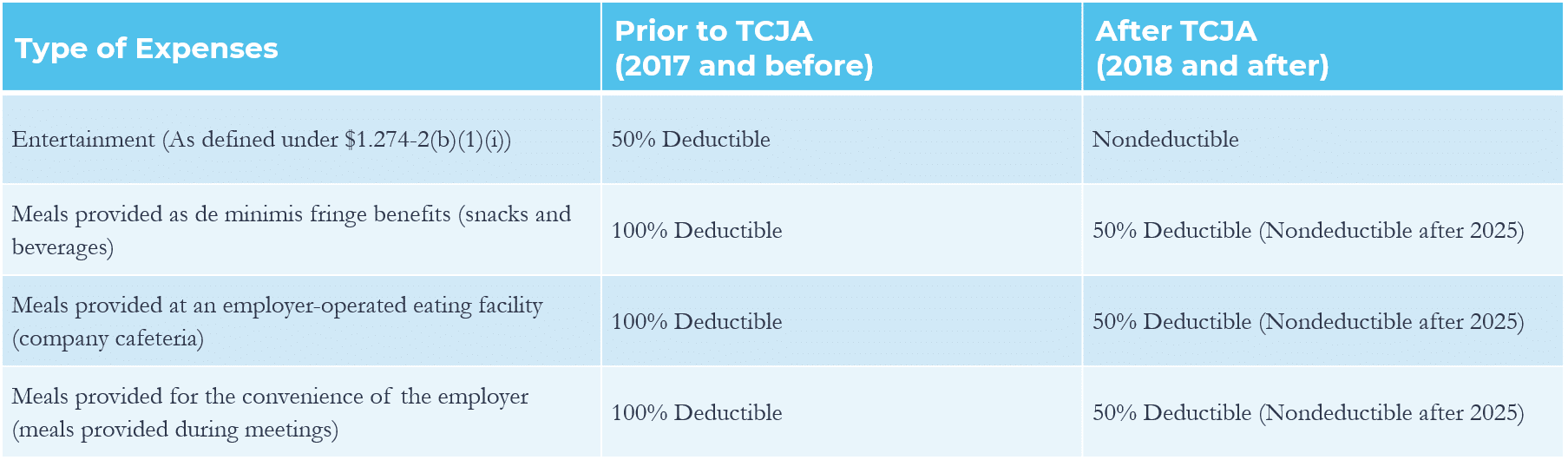

Navigating The New Meals And Entertainment Deductions Under Tcja Grf Cpas Advisors

The deductions allowed by section 162 which consist of expenses paid or incurred with respect to services performed by an official as an employee of a state or a political subdivision thereof in a position compensated in whole or in part on a fee basis.

Irc section 162 e. 162 e 2 b ii would be as follows. Read the code on findlaw. The organization of the internal revenue code as enacted in hundreds of public laws passed by the u s.

1163 6 apply to covered employees who retired before on or after the date of the enactment of this act oct. E section 162 a of the internal revenue code 26 u s c. 27 california generally conformed to irc section 162 with certain modifications.

62 a 2 d certain expenses of elementary and secondary school teachers. 162 e 1 c any attempt to influence the general public or segments thereof with respect to elections legislative matters or referendums or i r c. 162 e 1 d any direct communication with a covered executive branch official in an attempt to influence the official actions or positions of such official.

Congress since 1954 is identical to the organization of the internal revenue code separately published as title 26 of the u s. 28 irc section 162 m disallows a deduction for employee remuneration with respect to any covered employee to the extent that the amount of the remuneration for the taxable year for that employee exceeds 1 million. For example section 162 e 2 b ii 26 u s c.

The amendments made by this section shall not apply to instruments issued after july 10 1989 pursuant to a reorganization plan in a title 11 or similar case as defined in section 368 a 3 of the internal revenue code of 1986 if the amount of proceeds of such instruments and the maturities of such instruments do not exceed the amount or. Internal revenue code 26 usca section 162. Internal revenue code irc or the code 162 allows deductions for ordinary and necessary trade or business expenses paid or incurred during the course of a taxable year.

Rules regarding the practical application of irc 162 have evolved largely from case law and administrative guidance. Irc section 162 generally allows a deduction from gross income for ordinary and necessary expenses paid or incurred during the taxable year in carrying on any trade or business. It concerns deductions for business expenses.

Simpson Strong Tie Lus Zmax Galvanized Face Mount Joist Hanger For 2x4 Nominal Lumber Lus24z The Home Depot In 2020 Joist Hangers Wood Shed Plans Building A Deck

Deductibility Of Corporate Campaign Expenditures Everycrsreport Com

Lobbying Disclosure Reporting Deadline Approaches Which Method Do You Use A B Or C Political Law Briefing

Irc Section 162 Linked Benefit Executive Bonus Plans For Business Owners And Key Employees Bsmg

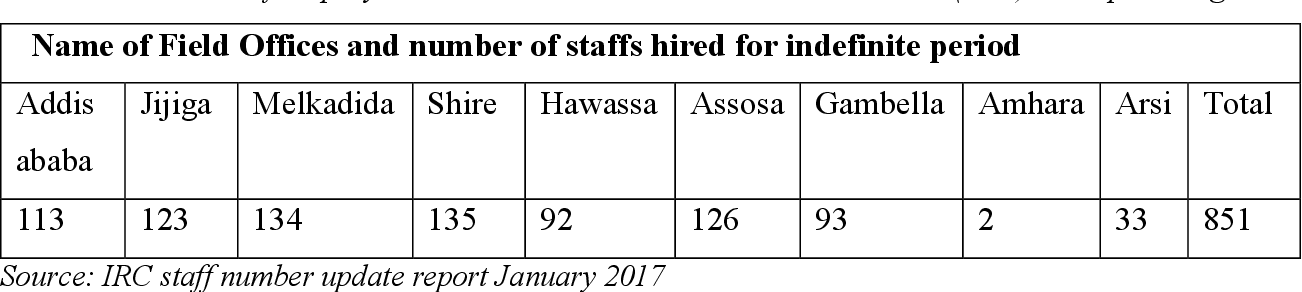

The Effect Of Reward On Employee Motivation In International Rescue Committee Irc Ethiopia Program Semantic Scholar

Https Highspeed1 Co Uk Media N00d1hcw Hs1 Ltd 5yams 30 May 2019 Final Update 12 July Pdf

Pin By Maxfin Investment On Sip Extra Money Financial Management Turn Ons

Nsr150sp Nsr150 Nsr 150 150sp 2stroke 2t Motorcycle Tygaperformance Tyga Repsol Irc Mobil

We Re All Mad Here The Mad Hatter Tattoo Mad Hatter Tattoo Body Art Tattoos Tattoos

Tax Reform S Effect On Lobbying Expenses Crowe Llp

Mobile Enlarged Screen Expander Amplifier New Bracket Stand Folding Phone 3d Unbranded New Mobile Phones Phone Screen Mobile Phone

4 10 8 Report Writing Internal Revenue Service

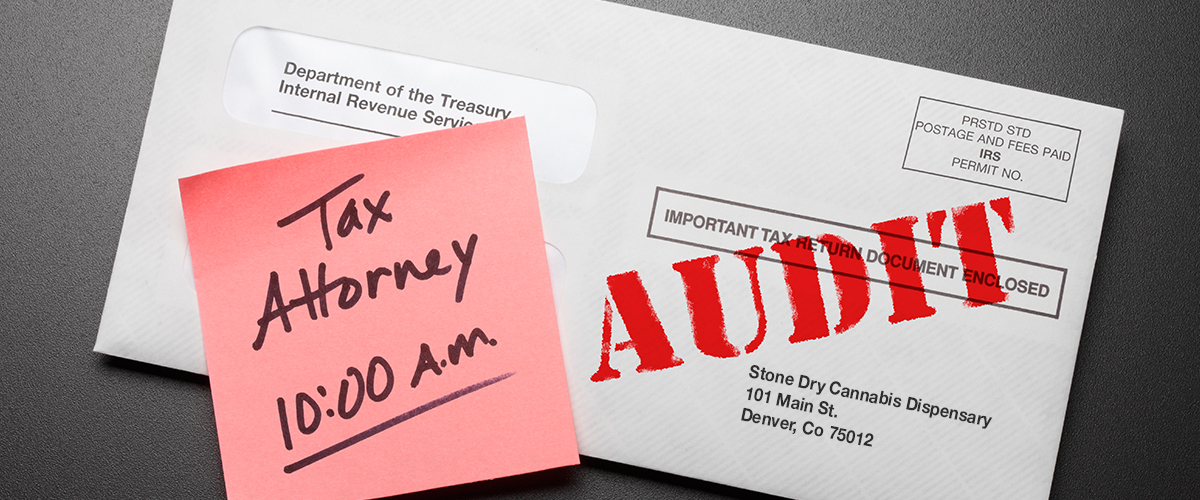

Another Cannabis Business Hit Hard By I R C Section 280e In U S Tax Court Cannabis Tax Attorney