Irc Section 404

Bsd 012 Moisture Control For New Residential Buildings Basement Construction Residential Building Building Construction

Code Tip Footing Drains And Foundation Waterproofing Greenbuildingadvisor Com Drainage Solutions Drainage Foundation Drainage

Doe Building Foundations Section 3 2 Concrete Wall Exterior Insulation In 2020 Exterior Insulation Building Foundation Waterproofing Basement

200 Sq Ft Tiny Home Floor Plan Design Floor Plan Design Tiny House Floor Plans House Floor Plans

Insulated Slab On Grade Basement With First Floor Detail Basement Insulation Basement Construction Waterproofing Basement

Rim Board Header Construction Construction Documents Architecture Details Joist Hangers

Amendment by section 404 d of pub.

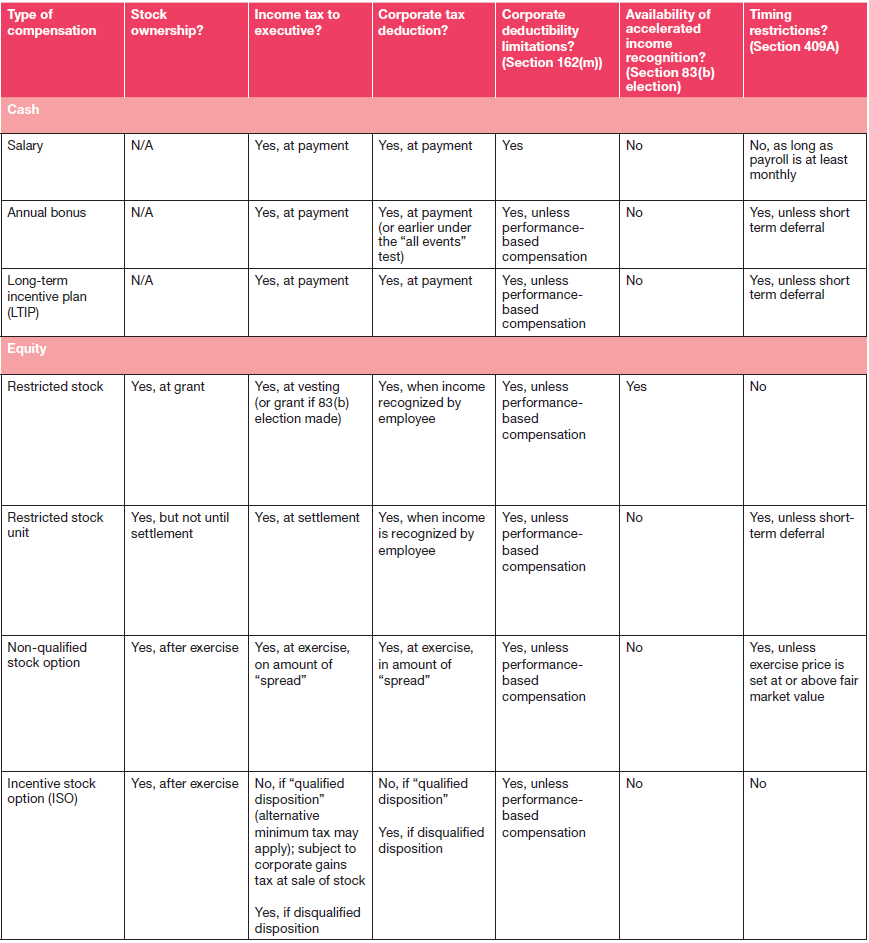

Irc section 404. For pre egtrra years tax years beginning before january 1 2002 the limitation was 15 of beneficiaries plan participant compensation. 108 311 set out as a note under section 45a of this title. Provisions of irc section 404 a 3 section 404 a 3 provides the deductible limits for profit sharing plans as well as stock bonus plans.

See irm 4 72 15 8 1 effective dates. Internal revenue code section 404 a 3 a i i deduction for contributions of an employer to an employees trust or annuity plan and compensation under a deferred payment plan. Section 404 c is a specific part of this law that permits employees to direct the investment of their own retirement accounts.

A for purposes of subsection g of section 404 of the internal revenue code of 1986 formerly i r c. 1954 relating to certain employer liability payments considered as contributions as amended by section 205 of this act any payment made to a plan covering employees of a corporation operating a public transportation system shall be treated as a payment described in paragraph 1 of such subsection if. 107 16 to which such amendment relates see section 404 f of pub.

The employee retirement income security act of 1974 erisa is a federal law that establishes the standards for private pension plans such as 401 k s and 403 b s. A plan under which the benefits are fixed or determinable limitations similar to those contained in clauses ii and iii of subparagraph a of section 404 a 1 determined without regard to the last sentence of such subparagraph a or. While this irm refers to regulations under 26 cfr 1 404 a 1 through 26 cfr 1 404 k 3 most haven t been updated for erisa and many other statutory changes.

The international code council icc is a non profit organization dedicated to developing model codes and standards used in the design build and compliance process. The international codes i codes are the widely accepted comprehensive set of model codes used in the us and abroad to help ensure the engineering of safe sustainable affordable and resilient structures. Section 404 a also governs the deductibility of unfunded pensions and death benefits paid directly to former employees or their beneficiaries see 1 404 a 12.

For taxable years beginning after 1962 certain self employed individuals may be covered by pension annuity or profit sharing plans. For purposes of section 446 of the internal revenue code of 1986 a determination under section 404 a 6 of such code regarding the taxable year with respect to which a contribution to a multiemployer pension plan is deemed made shall not be treated as a method of accounting of the taxpayer. The main reference for this irm section is irc 404 as amended through the csec act.

Ecological Education Freshwater Aquariums Aquarium Sump Aquarium Freshwater Aquarium

To Keep Basement Dry Finished Grade Should Slope Away From The Foundation For 10 Feet Minimum Foundation Drainage Patio Plans Drainage

Pin By Yuliya On Internal Basement Construction Insulated Concrete Forms Concrete Forms

Submersible Sump Pump Installed As Part Of An Internal De Watering System Waterproofing Basement Sump Pump Installation Sump Pump

Deck Planning Free Decking Guide Videos Q Deck Building A Deck Raised Deck Timber Deck

Book Cover Art Type 01 Book Cover Art Cover Art Types Of Art

Have Our Schools Become Re Segregated School Social Marketing Home Improvement Contractors

French Drains Drain Tile French Drain Downspout Drainage Backyard Drainage

Installing Deck Railing 5 Diy Deck Deck Railings Building A Deck

Ed Heck Cat And Mouse First Grade Art Art Art Projects

Grounding And Bonding Part 1 Of 2 Electrical Code Electrical Wiring Electricity

Hide Attic Door Google Search Attic Design Attic Access Door Attic Flooring

Vico Magistretti Lounge Chair For The Carimate Golf Club By Cassina 1960s Modern Retro Furniture Furniture Design Modern Scandinavian Chairs