Sample Section 754 Election Statement

Https Checkpointlearning Thomsonreuters Com Liveevent Download Location Prod Ecom H0191 Westlan Com Cpl Prod Marketing Webinarattachments 1369 12 29 16 20w238t Pdf Filename 12 29 16 20w238t Pdf

Making A Valid Sec 754 Election Following A Transfer Of A Partnership Interest

Section 754 And Basis Adjustments Pdf Free Download

Chapter 13 Basis Adjustments To Partnership Property Ppt Download

Https Www Drakesoftware Com Sharedassets Manuals 2017 Partnerships Pdf

Https Www Enterprisecommunity Org Sites Default Files Media Library Financing And Development Asset Management 2018 Tax Return Prep Guide Fiscal Year End Pdf

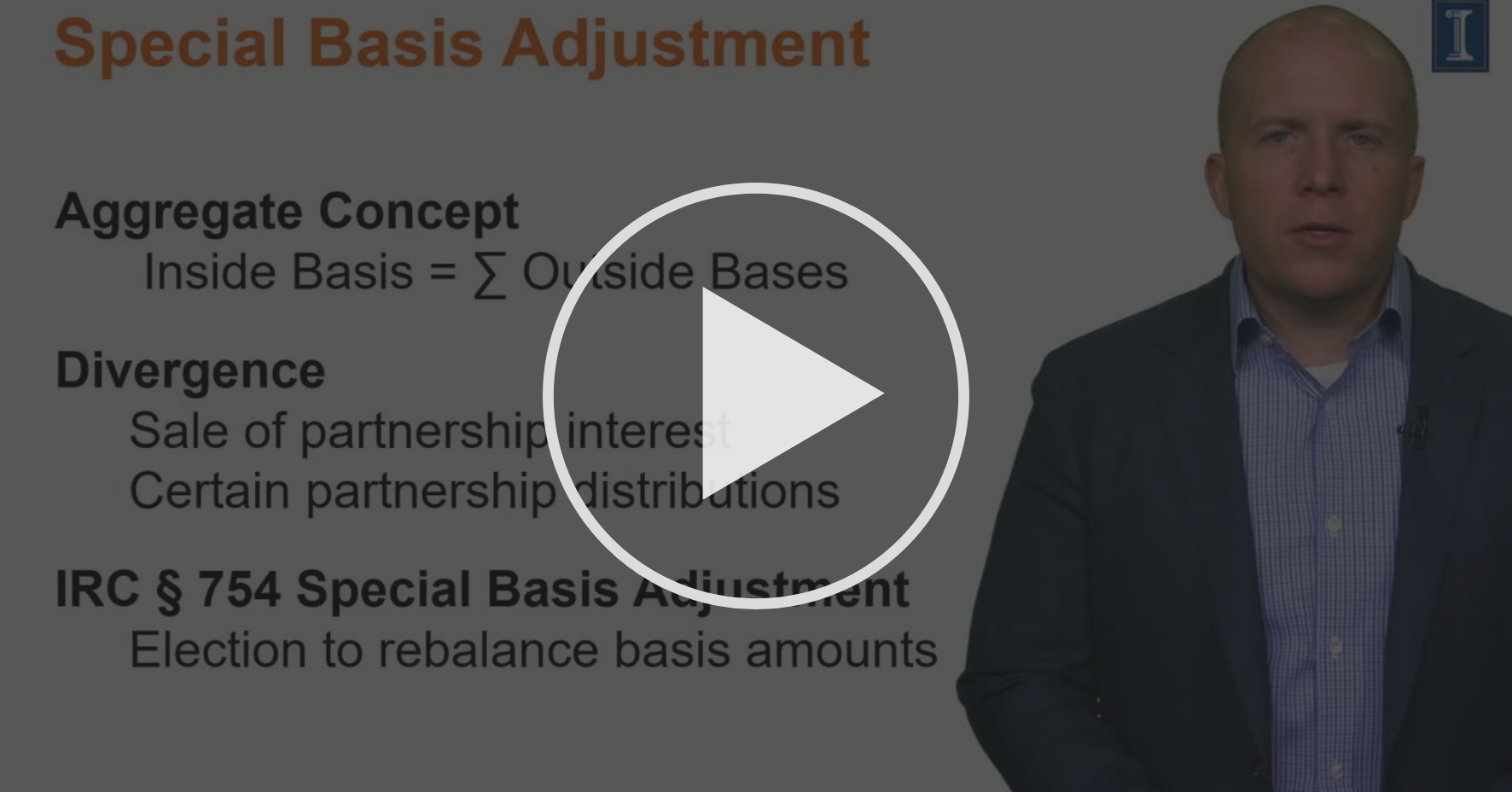

734 b and 743 b to adjust the basis of partnership property as provided by irc sec.

Sample section 754 election statement. Election to adjust the basis of partnership property under internal revenue code section 754 sample llc with 754 llc 235 n edgeworth st greensboro nc 27401 employer identification number. Pursuant to irc section 461 h 3 the s corporation hereby elects to adopt the recurring item exception as a method of accounting. A valid election under sec.

Election to adopt recurring item exception. Statement of section 754 election i. Two statements should be attached to the return for the taxable year during which the distribution or transfer occurs.

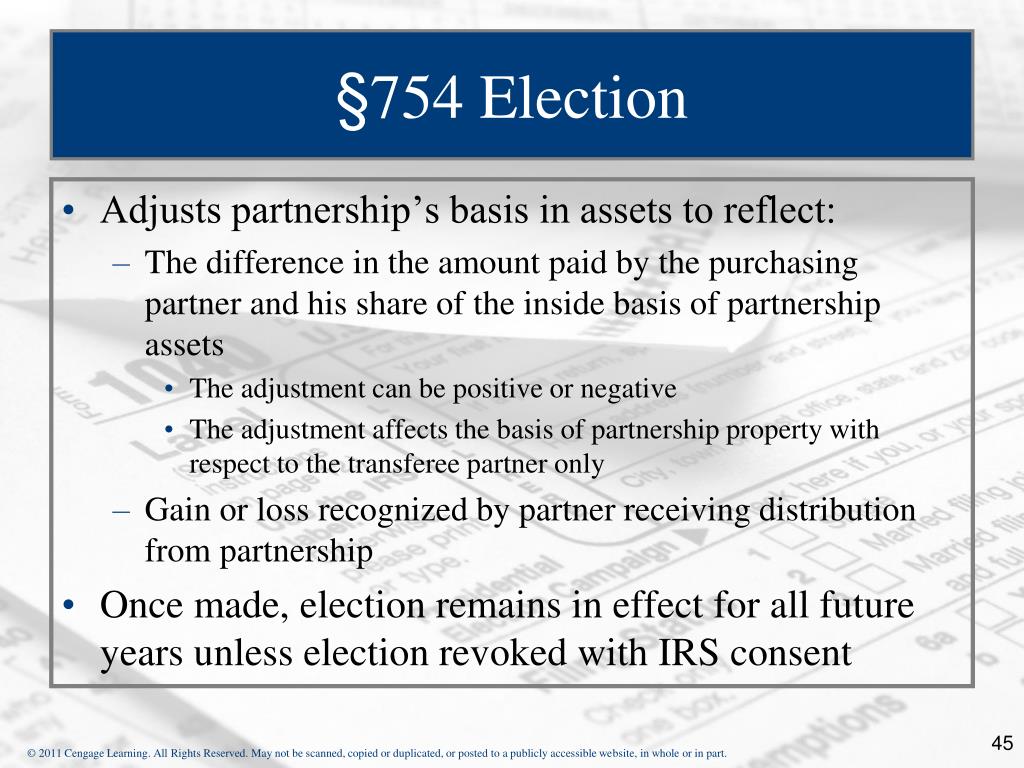

754 could substantially benefit the owners of entities treated as partnerships for tax purposes i e general partnerships limited partnerships limited liability companies limited liability partnerships and other multimember entities for which a check the box election was made to treat the entity as a partnership for tax purposes or for which the default classification in the absence of an election is to treat the entity as a partnership because it allows a. Pursuant to irc section 1 754 1 b 1 the partnership hereby elects to adjust the basis of the partnership property for the tax year ended 12 31 08. The purpose of a section 754 election is to reconcile a new partner s outside and inside basis in the partnership.

18 adopt recurring item exception sec 461 h 3 title. This will print an election statement. Partnership name partnership address.

Section 754 election 1065 only under section 754 a partnership may elect to adjust the basis of partnership property when property is distributed or when a partnership interest is transferred. Utilizing this election can accelerate deductions. 1 754 1 b 1 to apply the provisions of irc secs.

Section 754 provides that if a partnership files an election section 754 election in accordance with regulations prescribed by the secretary the basis of partnership property shall be adjusted in the case of a distribution of property in the manner provided in section 734 and in the case of a transfer of a partnership interest in the manner provided in section 743. The partnership referred to in this paragraph is. In the event of a transfer of all or part of the interest of a member at the request of the transferee or if in the best interests of the company as determined by the members as a major decision the company shall elect pursuant to section 754 of the code to adjust the basis of company property as provided by sections 734 and 743 of the code and any cost of such election or cost of administering or accounting for such election shall be at the sole cost and expense.

Https Www Thompsonhine Com Uploads 1136 Doc Domestic Taxable Mergers And Acquisitions Pdf

Sect 743 B Basis Adjustments On Partnership Interests Pages 1 50 Flip Pdf Download Fliphtml5

Https Www Houstoncpa Org Docs Librariesprovider2 Tax Expo 2020 205 345p Track 1 Overview Of Partnership Accounting And New Tax Return Reporting Updated Pdf Sfvrsn 143ac0b1 2

Lesson 4 2 1 Special Basis Adjustment Concepts Module 4 Partnership Sales And Terminations Coursera

Developments Affecting M A Deal Structure Ppt Download

Federal Register Limitation On Deduction For Business Interest Expense Allocation Of Interest Expense By Passthrough Entities Dividends Paid By Regulated Investment Companies Application Of Limitation On Deduction For Business Interest Expense

Consider Section 754 Election When Purchasing A Partnership Or Llc Interest Lexology

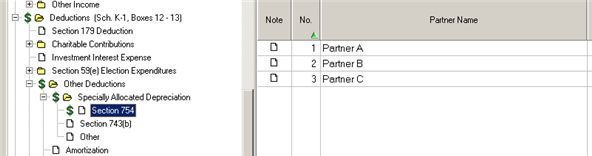

Entering Section 754 743 B Or Other Specially All Intuit Accountants Community

Advantages Of An Optional Partnership Basis Adjustment

424b3 1 Cnl 424b3 030718 Htm Prospectus Filed

Chapter 2 Partnership Interest Received For Contribution Of Property Ppt Download

Partnership Taxation What You Should Know About Section 754 Elections

Partnership Basis Inside Basis And Outside Basis