Section 125 Internal Revenue Code

Https Www Scgov Net Home Showdocument Id 35454

2019 Section 125 Plan Document Updates Core Documents

Ssa Poms Si 00820 102 Cafeteria Benefit Plans 07 23 2012

Maximize Your Tax Savings From Your Section 125 Plan American Fidelity

Irs Section 125core Documents

New Irs Guidance Provides Employers With Section 125 Plan Flexibility During 2020

Table of contents retrieve by section number.

Section 125 internal revenue code. Federal tax law begins with the internal revenue code irc enacted by congress in title 26 of the united states code 26 u s c. Section 125 f defines a qualified benefit as any benefit which with the application of 125 a is not includable in the gross income of the employee by reason of an express provision of chapter i of the internal revenue code other than 106 b 117 127 or l32. Fringe benefit exclusion rules.

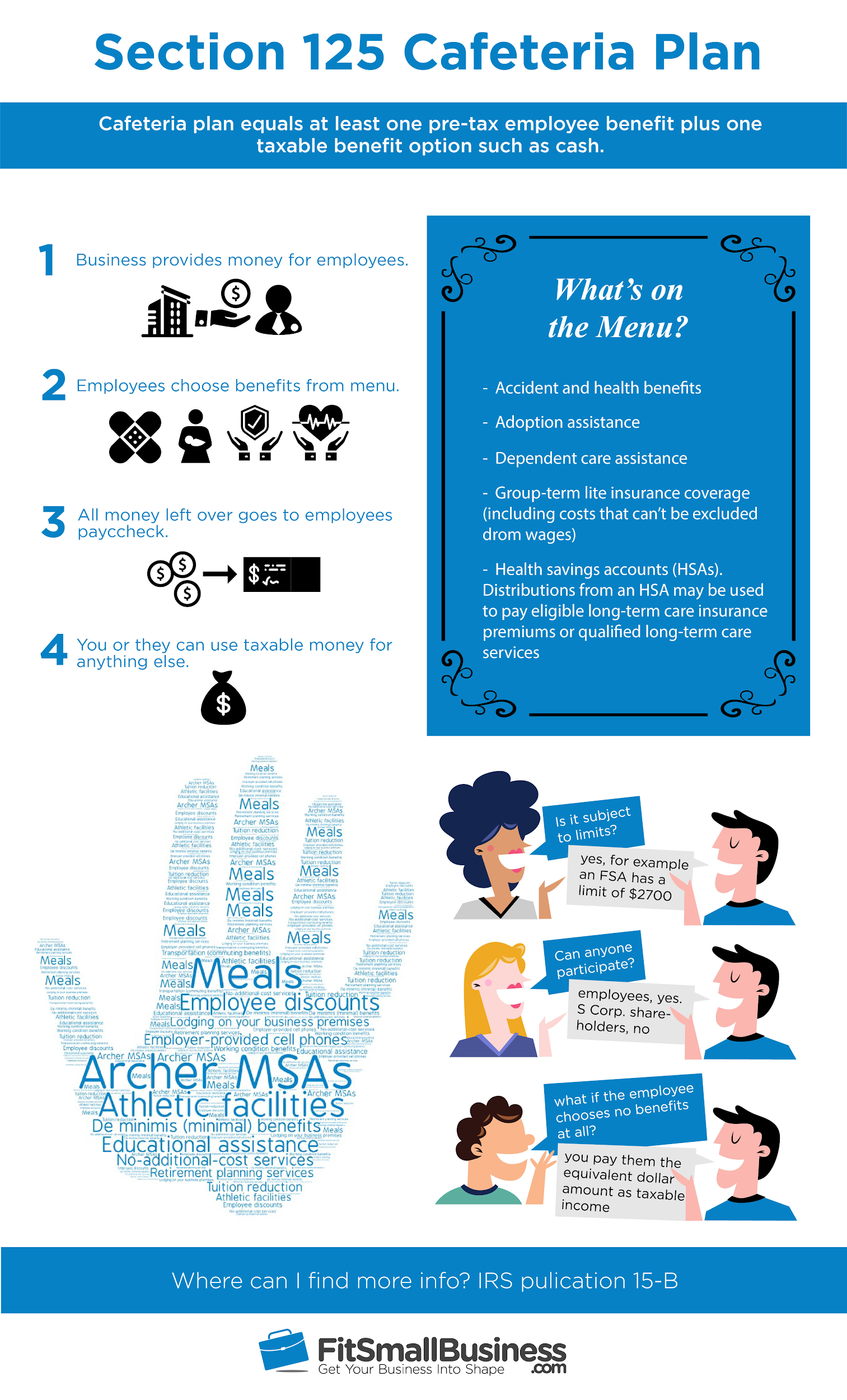

The plan is called a cafeteria plan because it includes a menu of benefits for employees to choose from. For provision that for purposes of section 125 of the internal revenue code of 1986 a plan shall not be treated as failing to be a cafeteria plan solely because under the plan a participant elected before january 1 1988 to receive reimbursement under the plan for dependent care assistance for periods after december 31 1987 and such assistance included reimbursement for expenses at a camp where the dependent stays overnight see section 10101 b 2 of pub. Section 125 of the internal revenue code refers to cafeteria plan benefits.

This notice provides guidance on the application of the rules under section 125 of the internal revenue code code relating to cafeteria plans including health and dependent care flexible spending arrangements fsas and section 223 of the code relating to health savings accounts hsas as those two provisions relate to the participation by same sex spouses in certain employee benefit plans following the supreme court decision in united states v. This section discusses the exclusion rules that apply to fringe benefits. Internal revenue code section 125 d 1 cafeteria plans.

These rules exclude all or part of the value of certain benefits from the recipient s pay. 100 203 as added by pub. Cafeteria plans on westlaw findlaw codes are provided courtesy of thomson reuters westlaw the industry leading online legal research system.

For more information about cafeteria plans see section 125 of the internal revenue code and its regulations. 100 203 as added by pub. For provision that for purposes of section 125 of the internal revenue code of 1986 a plan shall not be treated as failing to be a cafeteria plan solely because under the plan a participant elected before january 1 1988 to receive reimbursement under the plan for dependent care assistance for periods after december 31 1987 and such assistance included reimbursement for expenses at a camp where the dependent stays overnight see section 10101 b 2 of pub.

Internal revenue code 125. Except as provided in subsection b no amount shall be included in the gross income of a participant in a cafeteria plan solely because under the plan the participant may choose among the benefits of the plan. A plan does not fail to be a qualified benefits plan merely because it includes an fsa assuming that the fsa meets the requirements of section 125 and the regulations thereunder.

Section 125 Covid 19 Relief Irs On 2020 Mid Year Elections Fsa Claims Core Documents

Http Doa Alaska Gov Drb Pdf Employer Cafeteriaplans Slidesnoteshandout Pdf

Cafeteria Plan Section 125 Features Costs Providers

Is Your Section 125 Plan Compliant American Fidelity

Covid 19 Relief For Section 125 Plans And Increase In Fsa Carryover

What Is A Section 125 Pop Premium Only Plan Gusto

5 Things Districts Need To Know About Section 125 Cafeteria Plans

Understanding Section 125 Cafeteria Plans

Celebrating 40 Years Of Section 125 Cafeteria Plans Core Documents

Cafeteria Plan Options For 2020 Section 125 Pop Hsa Fsa Dcap Core Documents

Beware Of Free Or Self Serve Section 125 Plan Documents Core Documents

Https Www Dms Myflorida Com Content Download 140605 907025 Cafeteria Plan 2018 Pdf

Irs Courseware Link Learn Taxes