Section 2503 C Trust

Trust The Timing Of Your Life Quote Motivationalquote Movingonquote Prettyquote Lifequotes Pretty Quotes Taking Chances Quotes 25th Quotes

Sample Revocation Of Trust Form Blank Revocation Of Trust Example Template 8ws Templates Forms Living Trust Revocable Trust Document Templates

John Sample Trust Demo

Abcd Trust Model By Ken Blanchard A Great Leadership Tool Toolshero Leadership Ken Blanchard Trust In Relationships

Pdf Some Antecedents And Effects Of Trust In Virtual Communities

Speed Of Trust Transformation Process Organizational Culture Change Speed Of Trust Franklincovey Leadership Skill Trust Organizational

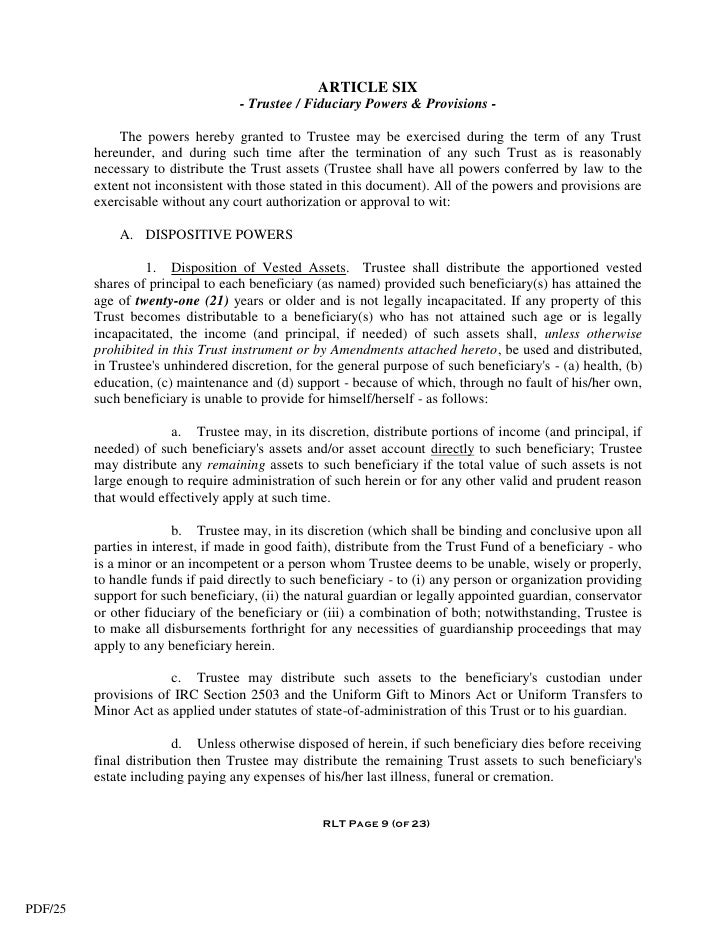

2503 c trust is a trust that complies with the requirements of sec.

Section 2503 c trust. Upon reaching majority the minor has full use and control over the assets. The property and the income may be expended for the minor s benefit. Section 2503 c trusts are called a minor s trust which is a separate legal entity that is established in order to hold gifts in trust for someone until they reach the age of 21.

The grantor of the trust cannot receive any income from the assets held in the trust. A section 2503 c trust allows all the principal and income to be used for the child until he reaches the age of 21 unlike the 2503 b trust that extends beyond age 21 and requires income to be paid to the child annually. The trustee can pay the child s college expenses from the 2503 c trust.

An irc section 2503 c trust is a gift tax tool that enables a grantor to make a gift to a minor in trust and still obtain the gift tax annual exclusion. The term taxable gifts means the total amount of gifts made during the calendar year less the deductions provided in subchapter c section 2522 and following. A section 2503c trust is a type of minor s trust established for a beneficiary under the age of 21 which allows parents grandparents and other donors to make tax free gifts to the trust up to the annual gift tax exclusion amount and the generation skipping transfer tax exclusion amount.

2503 c added in 1954 provides that a gift to a trust for the benefit of a minor is not a future interest if the trust meets three statutory requirements. The name comes from the internal revenue code that it is based upon. The trust derives its name from section 2503 c of the internal revenue code 26 u s c which sets down the requirements for the trust.

2503 c which grants an exception to the general rule that only gifts of a present interest qualify for the annual 15 000 gift tax exclusion for 2019 30 000 if gift splitting is elected. And 2 the passing requirement. The use of this irrevocable funded trust for gifts to minors eliminates many of the following practical objections to outright gifts.

2503 c trust is trust with only one beneficiary who must be a minor. Section 2503 c trust. B exclusions from gifts.

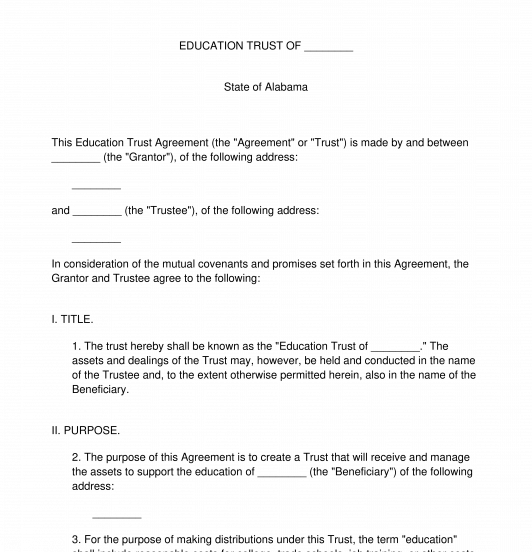

Education Trust Agreement Template Word Pdf

30 Quotes That Show Why Trust Is Everything In Relationships Friend Quotes Distance Trust Me Quotes Good Life Quotes

Trust Your Vibes Energy Never Lies Intuition Quotes Inspirational Quotes With Images Inspiring Quotes About Life

Trust Flowchart Revocable Living Trust Flow Chart Living Trust

2 503 Likes 55 Comments Max Lucado Maxlucado On Instagram Let S Strive For C A L M In 2018 W Max Lucado Quotes Inspirational Words Spiritual Quotes

I Promise I Will Never Make You Feel Like You Can T Trust Me I Will Be An Open Book So You C Trust Yourself Quotes Broken Trust Quotes Trust In Relationships

Trust The Reroute Quote Wallpaper In 2020 Wallpaper Quotes Quotes Mantras

Pin By Sheri On Quotes In 2020 Trust Quotes Hd Quotes Friendship Quotes

Trust The Wait Words Quotes Caption Quotes Words

If You Break My Trust It S Up To Me When If Ever I Trust You Again Not You You Broke Me Trust Yourself Im Me Quotes

Pdf Value Co Creation And Trust In Social Commerce An Fsqca Approach

Trust No One Tattoo Sketches Calligraphymasters Calligritype Calligraphy Thedailytype Goodt Typography Tattoo Writing Tattoos Tattoo Lettering Styles

Pin By Flavio A A De Lima On Stamps That I Like Postage Stamp Design Design Stamps Stamp Design