Section 3401 A Wages Definition

Http Www Irs Gov Pub Irs Wd 9903032 Pdf

What Is A Blue Chip Commodity Trading Trading Option Trading

The Federal Income Tax Capital Vs Income

Https Www Vcera Org Sites Main Files File Attachments Resolution Of The Bor Of Vcera Pertaining To Regulations Of Internal Revenue Code 415 Annual Limits Pdf 1515434031

Https Www Irs Gov Pub Irs Wd 9938013 Pdf

Every Which Way But Loose Iii

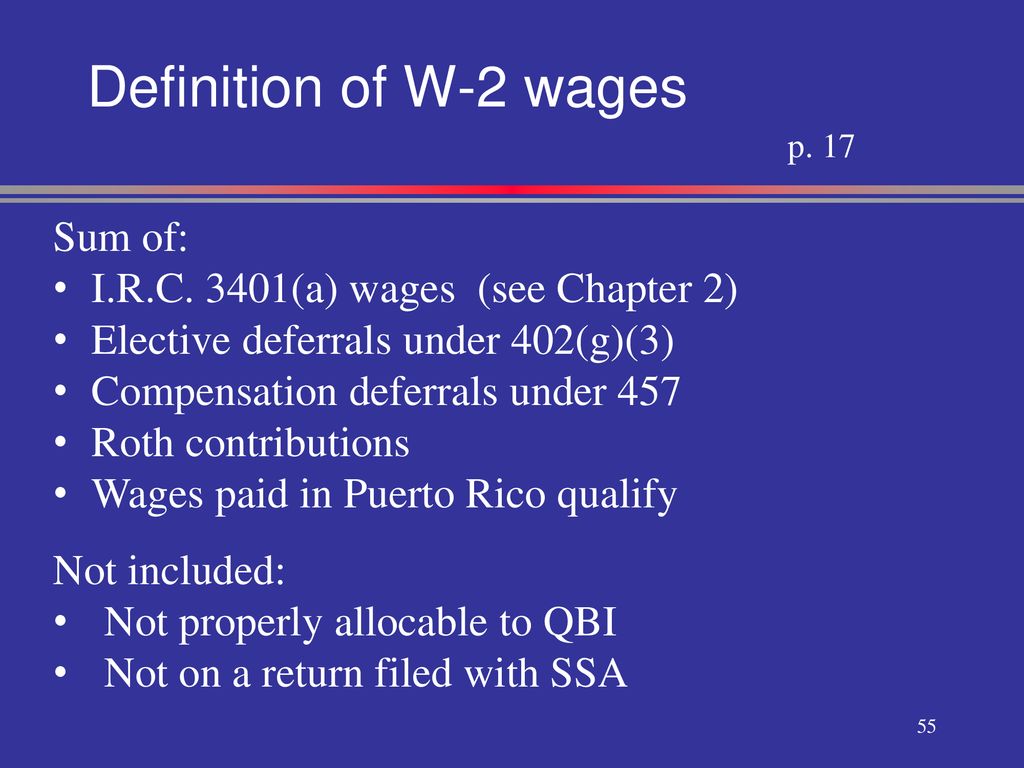

However because certain income is exempt from income tax withholding not all w 2 wages should be included in 3401 a wages.

Section 3401 a wages definition. Includes net income for sole proprietors and partners. Along with w 2 compensation section 3401 a wages are an alternative safe harbor definition of compensation meaning that this definition can be used to calculate the 415 limit as well as related compliance limits. Code section 3401 a wages.

Section 31 3401 a 1 a 2 provides that the name by which remuneration for services is designated is immaterial. Code section 3401 a wages. Code section 3401 a wages.

All possible compensation items are described below but only those compensation items allowed by your plan should be used for plan purposes. Code section 3401 a provides the definition compensation for federal income tax wage withholding for retirement plan purposes. So all compensation included in 3401 a wages would also be included in w 2 wages.

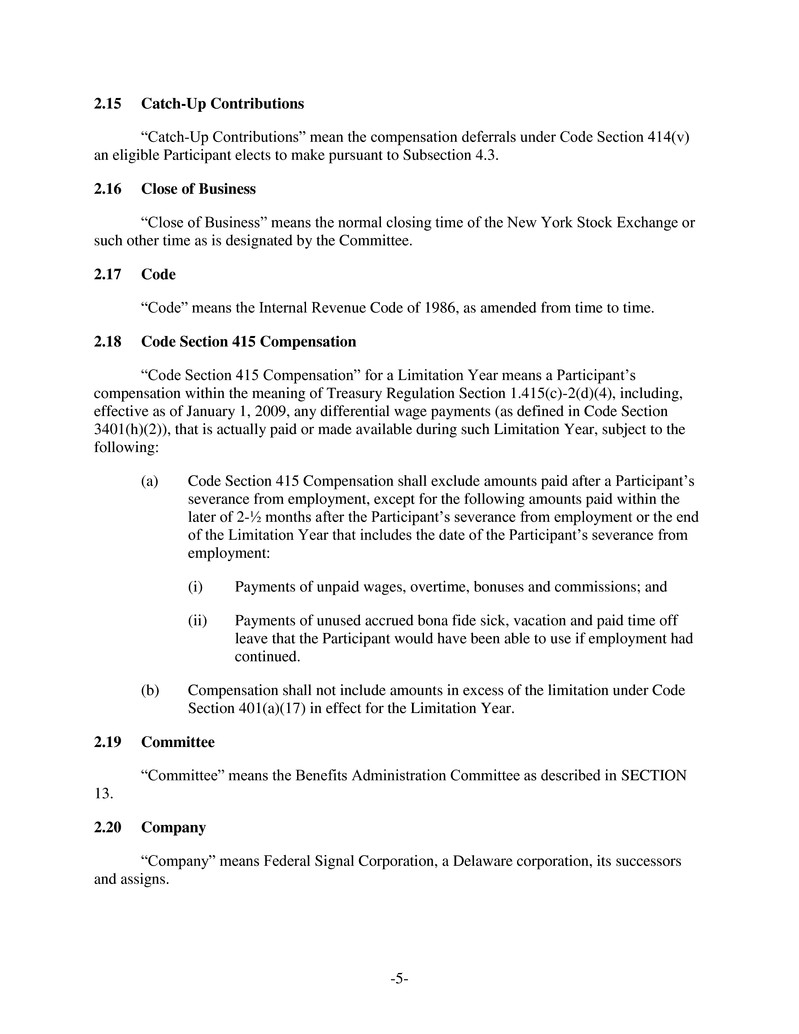

415 c compensation is defined as wages within the meaning of code section 3401 a for purposes of income tax withholding at the source but determined without regard to any rules that limit the remuneration included in wages based on the nature or location of the employment or the services performed such as the exception for agricultural labor in code section 3401 a 2. For purposes of this chapter the term wages means all remuneration other than fees paid to a public official for services performed by an employee for his employer including the cash value of all remuneration including benefits paid in any medium other than cash. 415 safe harbor compensation.

These are wages reported on form w 2. Wages salaries and fees for professional services rendered in the course of employment. Except that such term shall not include remuneration paid.

Code section 3401 h 2 made by an employer while on active duty w uniformed services for a period of more than 30 days and represents all portion of the wages the individual would have received if the individual were performing service for the employer treated as wages for tax purposes. Except that such term shall not include remuneration paid. A wagesfor purposes of this chapter the term wages means all remuneration other than fees paid to a public official for services performed by an employee for his employer including the cash value of all remuneration including benefits paid in any medium other than cash.

Feminism 101 An Introduction Kanishka Sikri Feminism Words Faith In Humanity

Exhibit10r

Https Persi Idaho Gov Documents Retirees Choice Plan Legal Document Pdf

Pin On David Posel

Nigeria Nigeria Selected Issues And Statistical Appendix

Http Www Tax Freedom Com The 20book 20of 20john Pdf

Https Www Scers Org Sites Main Files File Attachments 20191218 Item 13 Pdf

Qbi Non Sstb Chapter 1 Pp Ppt Download

Restatement Of The Sallie Mae 401 K Savings Plan Effective Slm Corp Business Contracts Justia

Http Losthorizons Com Tax Taximages2 Dennisgfed2012docs Pdf

Volunteer Work As A Valuable Leisure Time Activity A Day Level Study On Volunteer Work Non Work Experiences And Well Being At Work Mojza 2011 Journal Of Occupational And Organizational Psychology Wiley

Https Home Treasury Gov System Files 131 File 2a Application For Benefit Suspension Exh 17 Redacted Pdf