Section 409a Summary

Https Www Friedfrank Com Sitefiles Publications 4051c4d3cdccafea809ecfdb7a31e0ad Pdf

Know Your Valuation For Equity Compensation And Avoid The Perils Of

Section 409a Top 10 Rules For Compliant Non Qualified Deferred Compensation

Https Www Sec Gov Divisions Corpfin Cf Noaction 2007 Hcc061207 13e 4 Incoming Pdf

409a Guidance On Nonqualified Deferred Compensation Plans For Beginne

What Is A 409a Valuation Carta

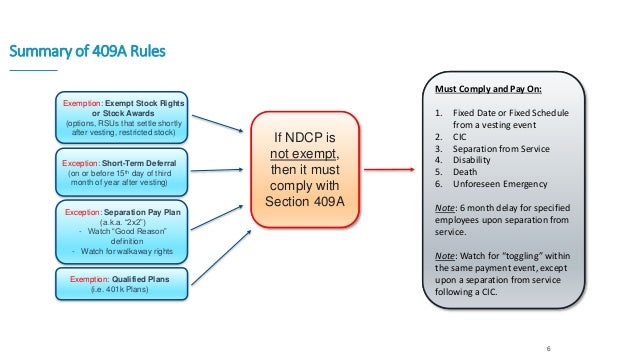

The regulations provide a definition of a nonqualified deferred compensation plan subject to section 409a including rules related to the statutory effective date and rules governing initial and subsequent deferral elections the establishment of the time and form of payment.

Section 409a summary. Or c used or relied upon for any purpose other than as a general overview and summary of section 409a and its likely application to the specified agreements. Service recipients are generally employers but those who hire independent contractors are also service recipients. It created a new section 409a of the internal revenue code 409a and the code respectively.

Notwithstanding section 885 d 1 of the american jobs creation act of 2004 pub. A used or relied upon by or quoted or delivered to any other person. 409a affects nonqualified retirement plans and other deferred compensation arrangements.

Section 409a of the united states internal revenue code regulates nonqualified deferred compensation paid by a service recipient to a service provider by generally imposing a 20 excise tax when certain design or operational rules contained in the section are violated. On the positive side section 409a resolves decades of uncertainty created by conflicts between irs positions and federal court authority. We are not attorneys so we will leave the legal minutiae of that definition for others to grapple with noting only that generally speaking a deferred compensation plan is an arrangement whereby an employee service provider in 409a parlance receives compensation in a later tax year.

108 357 provided the following. Section 409a defines nqdc as a legally binding right to compensation that is payable and taxable in a later tax year. B reproduced or filed publicly.

On the negative side. The following is a summary of ten principles that are central to understanding the scope and impact of section 409a. 108 357 set out below subsection b of section 409a of the internal revenue code of 1986 shall take effect on january 1 2005.

Not later than 90 days after the date of the enactment of this act the secretary of the treasury shall issue guidance on what constitutes a change in ownership or effective control for purposes of section 409a of the internal revenue code of 1986 as added by this section. The definition of deferred compensation is very broad causing sec. Broad impact on executive compensation arrangements.

Notice 2010 6 Summary Required 409a Document Provisions Pages 1 3 Text Version Anyflip

409a Nonqualified Deferred Compensation Plans The Hartford

Section 409a Valuations Dla Piper Accelerate

Irc 409a Overview 409a Valuations Explained Equityeffect

United Health Group Pdf Document Earnings Release Final Financial

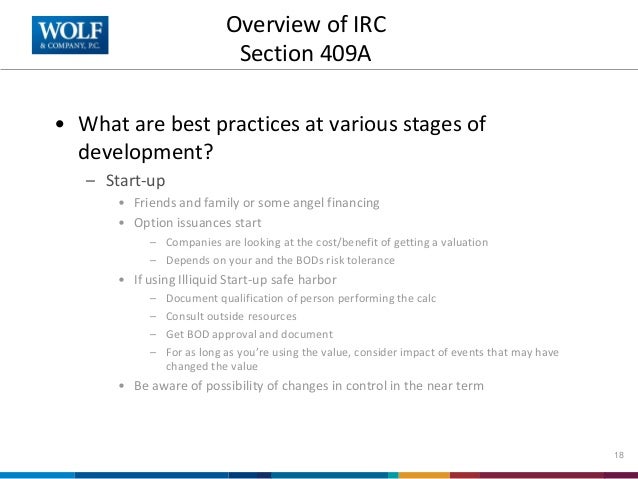

Jennifer Bibart Dunsizer Ppt Download

Business Valuation For Start Ups Business Fundamentals Bootcamp March 6 Ppt Download

A Question And Answer Guide To Internal Revenue Code Section 409a Lexology

Exhibit101offerlettertot

Document Vectrus Inc 2018 Current Report 8 K

Exhibit993fnhcrestricted

Exhibit992fnhcrestricted

Section 409a Handbook Second Edition Bloomberg Law Books