W2 Section 125

How To Decode Box 1 Of Form W 2 Tricore

Understanding Your W 2 Controller S Office

Quick Reference Guide For The Paycor W 2

Box 12w Hsa Employer Contributions Asap Help Center

Irs Courseware Link Learn Taxes

02 02 16 W 2 Form For Calendar Year 2015 Almanac Vol 62 No 21

An employee can generally exclude from gross income up to 5 000 of benefits received under a dependent care assistance program each year.

W2 section 125. The amount has already reduced your w2 box 1 wages so you don t deduct it again on your federal return. This may sound like it has something to do with where you go on your lunch break but there is a more reasonable explanation. They are not taxed and are not included in your w 2 box 1 wages so you can not deduct them as medical expenses.

It is also known as a cafeteria plan. Y deferrals under a section 409a nonqualified deferred compensation plan. How is this benefit reported on form w 2.

From a section 125 cafeteria plan. A section 125 plan is part of the irs code that enables and allows employees to take taxable benefits such as a cash salary and convert them into nontaxable benefits. The plan is called a cafeteria plan because it includes a menu of benefits for employees to choose from.

Adding in box 14 doesn t go anywhere or do anything. The benefits received by an employee exceed 5 000. Report on form 8889 health savings accounts hsas.

Hence when providing compensation data on the census for plan compensation it is important for the plan sponsor to understand that pre tax contributions to section 125 and 129 plans are not taxable for medicare but they are part of a participant s gross compensation so the amount on box 5 of the w 2 or the w 3 medicare wages does not represent plan compensation even when the base definition listed is w 2 wages. This amount is a reported in box 1 if it is a distribution made to you from a nonqualified deferred compensation or nongovernmental. Complete form 2441 child and dependent care expenses to compute any taxable and nontaxable amounts.

These benefits may be. If your employer has enrolled you in a s125 plan they may notate this on box 14 of your w 2 using the term s125. Any amount over 5 000 also is included in box 1.

What Is S125 On A W 22

What Is Cafe 125 On A W 2 Tax Form Turbotax Tax Tips Videos

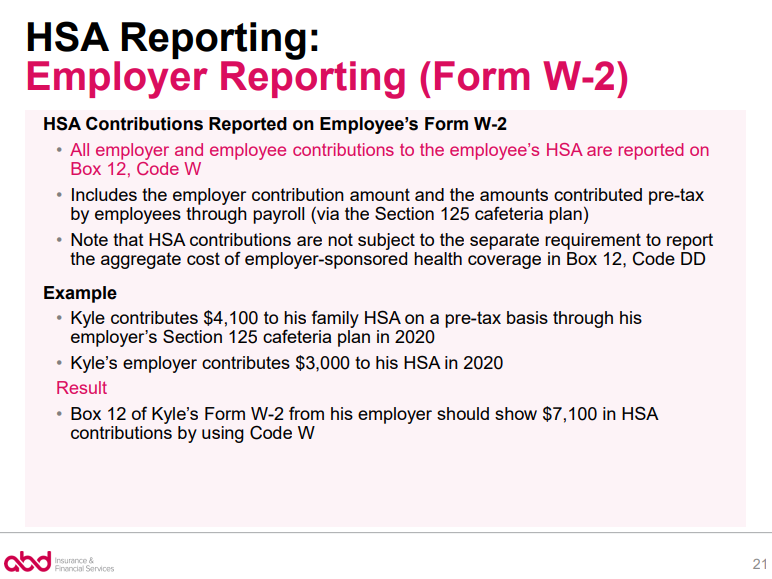

Hsa Form W 2 Reporting Abd Insurance Financial Services

So You Have Stock Compensation And Your Form W 2 Just Arrived Now What The Mystockoptions Blog

W2 Tax Return Google Sok

How To Read Your W 2 Form To Correctly File Your Tax Returns

Printable And Fileable Form 1099 Misc For Tax Year 2017 This Form Is Filed By April 15 2018 Fillable Forms Irs Forms 1099 Tax Form

Http Doa Alaska Gov Drb Pdf Employer Cafeteriaplans Slidesnoteshandout Pdf

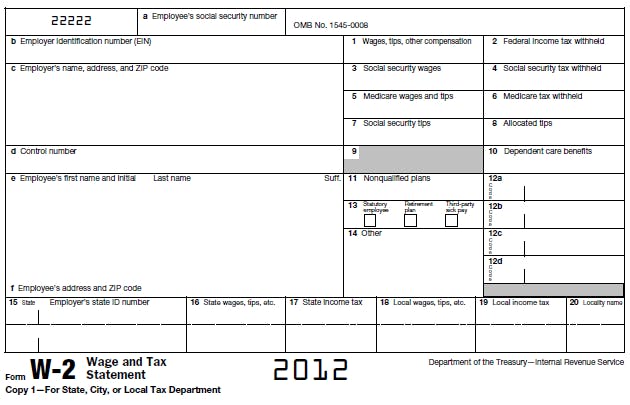

2012 Form Irs W 2 Fill Online Printable Fillable Blank Pdffiller

Pay Codes Tab

W 2 Wage Tax Statement Hostos Community College

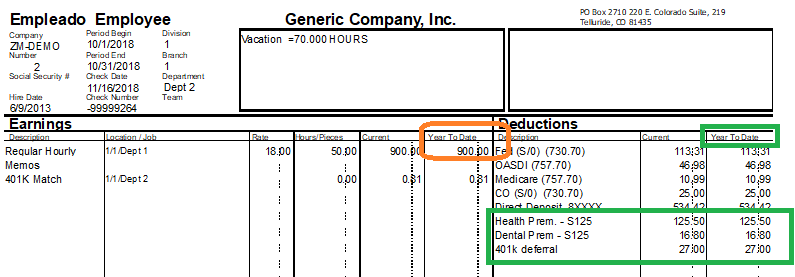

Why Are W 2s And Final Pay Stubs Different Aps Payroll

What Is A Section 125 Pop Premium Only Plan Gusto