Duty Drawback Under Section 75

Drawback Of Duty Customs Act Ppt Download

Duty Drawback Hand Book 2018 Customs Excise Free 30 Day Trial Scribd

Duty Drawback Claim Procedures

Procedures To Claim Drawback After Gst Implantation

Duty Drawback Scheme

Export Promotion Schemes Ppt Video Online Download

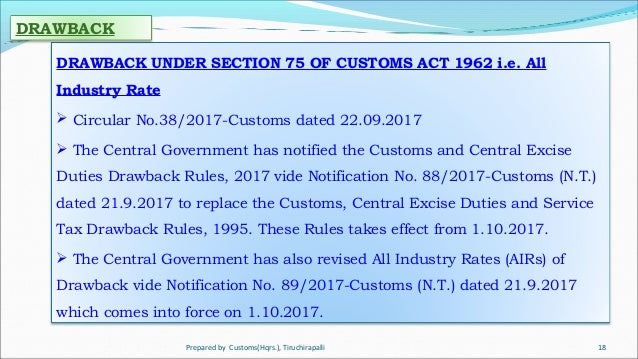

Under gst regime drawback under section 75 shall be limited to customs duties on imported inputs and central excise duty on items specified in fourth schedule to central excise act 1944 specified petroleum products tobacco etc used as inputs or fuel for captive power generation.

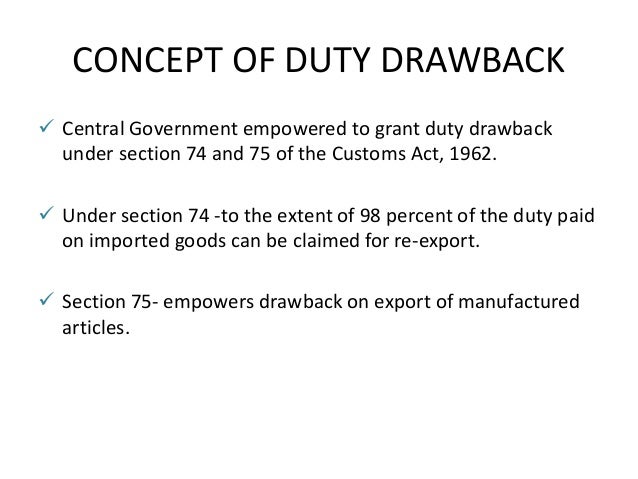

Duty drawback under section 75. Whereas section 75 allows drawback on imported goods used in the manufacture of export goods. The duty drawback provisions are described under section 74 and section 75 under the customs act 1962. The central government is empowered to grant duty drawback under section 74 and 75 of the customs act 1962.

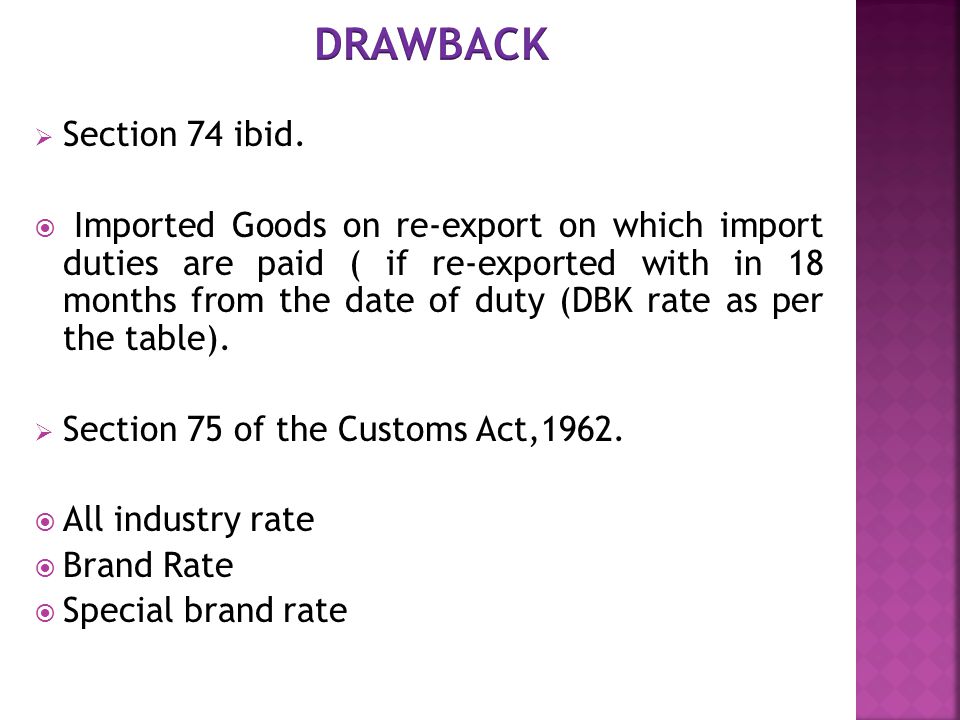

Categories of duty drawback. Duty drawback provisions are given under section 74 and 75 of the customs act 1962. This act laid down the various restrictions and conditions to claim drawback of duties under certain situations.

A new section 75 a has been incorporated in the customs act to provide for payment of interest on delayed payment of drawback. Interest at the rate of 15 p a. Section 75 of the customs act 1962 duty drawback u s 74 duty drawback u s 75 when admissible imported goods are exported as such without being used or after use imported goods are used in manufacture of goods which are exported related rules re export of imported goods duty drawback of customs duties rules 1995.

Interestingly when there is erroneous recovery of drawback under rule 16 of drawback rules 1995 or recovery under rule 16 a is contemplated rate of interest of 15 is fixed under section 28 aa is applicable. Drawback under section 75 the term draw back has been defined in rule 2 a duty drawback rules 1995 to mean in relation to any goods manufactured or processed. The central government may make rules for the purpose of carrying out the provisions of sub section 1 and in particular such rules may provide 8 a for the payment of drawback equal to the amount of duty actually paid on the imported materials used in the manufacture or processing of the goods or carrying out any operation on the goods or as is specified in the rules as the average.

Drawback on imported materials used in the manufacture of goods which are exported. In order to facilitate the drawback procedures the central government is empowered to make rules. Section 75a 1 of the customs act stipulate that in case of delayed payment of drawback under section 74 and 75 of the act interest at the rate of 6 prescribed under section 27a will be applicable here interest accrued after expiry of one months.

In this article we look at the procedure for claiming duty drawback of export in india. Under section 74 of the customs act 1962 duty drawback to the extent of 98 percent of the duty paid on imported goods can be claimed for re export provided the goods are re exported within two years of payment of import duty. Section 74 allows duty drawback on re export of duty paid goods.

Bringing S75 Consumer Credit Act Claims Against Banks Is It Still Justifiable Legal Cheek

Commission Implementing Regulation Eu 2015 2447 Of 24 November 2015 Laying Down Detailed Rules For Implementing Certain Provisions Of Regulation Eu No 952 2013 Of The European Parliament And Of The Council Laying Down

Duty Drawback For Export An Incentive Scheme Interpreted Right For You

Refund Claim Of Safeguard Duties As Duty Drawback

Https Ec Europa Eu Taxation Customs Sites Taxation Files Docs Body Guidance Special Procedures En Pdf

Uk Trade Tariff Excise Duties Reliefs Drawbacks And Allowances Gov Uk

Annexure Ii Form For Claim Of Drawback

Custom Benefits Meis Seis Aa And Epcg Services Greenvissage

Consumer Credit Act Why You Ve Got Rights Under Section 75 Which Conversation

Exports Under Gst Presentation Uploaded

How To Claim Brand Rate Of Drawback

Concept Of Duty Drawback

Recovery Of Drawback Amount Under Rule 18 Of Drawback Rules 2017