Home Loan Interest Deduction Under Section 24 B

Income Tax Deductions List Fy 2019 20 List Of Important Income Tax Exemptions For Ay 2020 21 Tax Deductions List Tax Deductions Income Tax

Home Loan Tax Benefits And Exemptions That You Can Avail Finance Loans Loan Investing

Common Deductions And Exemptions Investing Deduction Income Tax

Income Tax Deductions List Fy 2018 19 List Of Important Income Tax Exemptions For Ay 2019 20 Tax Deductions List Tax Deductions Income Tax

Section 80eea Eligibility Rebate Applicability Period Total Benefit Housing News

Income Tax Deductions List Fy 2019 20 List Of Important Income Tax Exemptions For Ay 2020 21 Tax Deductions List Tax Deductions Income Tax

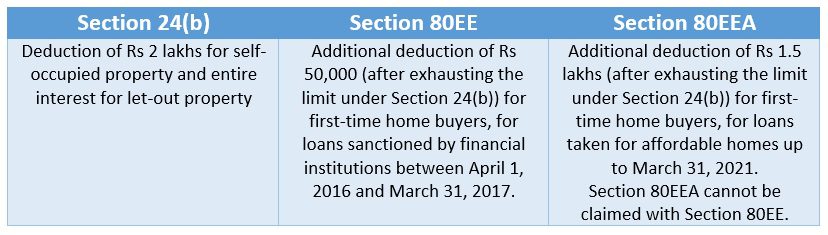

Under the provisions of the section home buyers can save an additional rs 1 50 lakhs per year towards the interest paid on home loans over and above the rs 2 lakhs that they already save under section 24 b.

Home loan interest deduction under section 24 b. In respect of self occupied house property interest deduction u s 24 b is restricted to rs 2 00 000. It is over and above the deduction of rs 2 00 000 available under section 24 b for interest paid in respect of loan borrowed for acquisition of a residential house property. As per explanation given to section 24 b deduction of house loan interest payable by the assessee in previous year in which such property has been acquired or constructed will be deducted in five equal annual installments commencing from the previous year in which the house is acquired or constructed.

For a self occupied house property since the annual value is nil the standard deduction is also zero on such a property. Maximum deduction allowed under this section is rs 1 50 000. B deduction of interest on home loan for the property homeowners can claim a deduction of up to rs 2 lakh rs 1 5 lakh if you are filing returns for fy 2013 14 on their home loan interest if the owner or his family.

Two new sections 80ee and 80eea have been introduced in the act one by finance act 2016 and the other by way of finance act 2019 which deals with the deduction of interest over and above section 24 b. Section 24 section 24 of the income tax act deals with interest that an individual pays on home or property loans. The deductions available are loan interest and standard deduction.

However interest deduction for pre acquisition or pre construction period is also allowed but only after acquisition or construction is complete. In case the house is in the joint name of your spouse and you joint loan each one can avail of rs2 lakh interest component deduction. It is allowed in 5 equal annual installments.

Such loan should be taken for purchase or construction or repair or reconstruction of house property. Also only the interest on home loan is allowed as deduction u s 24 b and not the interest on interest. In other words the interest payable for the year is allowed as deduction whether such interest is actually paid or not.

Interest deduction on housing loans under section 24 b on the other hand is allowed only on acquisition or completion of the house property. Interest paid on housing loan is allowed as a deduction to the extent of rs 2 lakhs in respect of self occupied property. The interest component of home loans is allowed as deduction under section 24 b for up to rs2 lakh in case of a self occupied house.

Understanding Your Form 16 Income Tax Return Income Tax Filing Taxes

Accounting Taxation Income Tax Deductions Lic Donation Mediclaim Pension Fund Home Loan Repayment Bank Fdr Etc Carry Tax Deductions Income Tax Income

Accounting Taxation Interest Rates Of Delay In I T Returns Submission I T Returns Non Submission Failure To Income Tax Return Interest Rates Pay Advance

Planning To Buy A Home In 2015 Here Are Some Tips That Will Help You Plan Your Finances To Avail Details On Home Loa Home Buying Home Buying Tips Home Loans

Accounting Taxation Income Tax Deductions Lic Donation Mediclaim Pension Fund Home Loan Repayment Bank Fdr Etc Pension Fund Tax Deductions Tax Refund

Even With Higher Income Of Rupees 12 75 Lakh You Can End Up Paying No Income Tax At All Budget 2019 Has Brought Many Things To Income Tax Budgeting Income

Income Under The Head House Property With Questions And Answers Accounting Taxation Income This Or That Questions House Property

Home Loan Tax Benefits Under Section 80 Eea In Budget 2019 Rs 1 5 Lakh Additional Tax Deduction On Affordable Housing Loans Tax Deductions Home Loans Budgeting

How To Save Tax On Rental Income In India Tax Deductions On Rent

Tax Planning For Salaried Individual Accounting Taxation How To Plan Tax Refund Tax

Reducing Tax Burden Different Sections Like 80c 80d Etc Detailed Infographic By Livemint Incometax Public Provident Fund Tax Deductions Tuition Fees

Routine Of Some Positive Habits Always Pull Oneself Towards Success Here Is A List Of Some These Financial Habits Tha Business Loans Small Business Loans Loan

Section 24 Tax Deduction Under Section 24 For Home Owners Abc Of Money