Section 382 Ownership Change

Is It Time For A Section 382 Study The 5 Questions You Must Ask To Find

Section 382 And Limited Net Operating Losses

Valuation Considerations Of Section 382 Limitations Vrc

Fuel Injector Automotive Repair Engineering Automobile Engineering

What Businesses Need To Know About Section 382 And Other Changes To Net Operating Loss Rules San Francisco Business Times

Accounting For And Classification Of Special Tools Referred To As Tooling Dreport In English

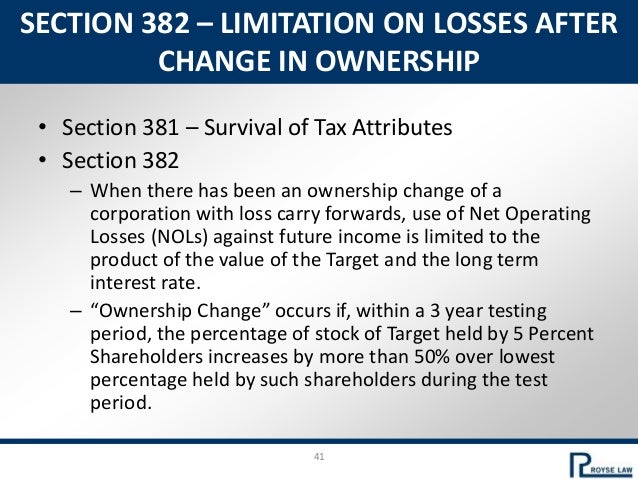

There are two main components of this section which are limitation and ownership change.

Section 382 ownership change. When there is an ownership change the corporation is now considered to be a new loss corporation and it is subject to the section 382 limitations. Ownership change happens when it s a loss corporation and after the end of the testing date the stock percentage of the business owned by 1 or 5 shareholders has increased by 50 points. An ownership change is defined generally as a greater than 50 change in the ownership of stock among certain 5 shareholders over a three year period sec.

A section 382 ownership change generally occurs if the percentage of the stock of. Section 382 together with section 383 generally affects corporations that undergo a greater than 50 change in ownership during any three year period and that have significant net operating loss. Convertible preferred stock certain convertible debt instruments common stock and stock options.

Stock includes the following. 382 to limit the use of corporate nols following an ownership change. Accordingly an ownership change occurs as a result of the merger.

Section 382 l 3 c provides that except as provided in regulations any change in proportionate ownership of the stock of a loss corporation attributable solely to fluctuations in the relative fair market values of different classes of stock shall not be taken into account. If during the 2 year period immediately following an ownership change to which this paragraph applies an ownership change of the new loss corporation occurs this paragraph shall not apply and the section 382 limitation with respect to the 2nd ownership change for any post change year ending after the change date of the 2nd ownership change shall be zero. On september 9 2019 the treasury department treasury and the internal revenue service irs proposed regulations proposed regulations addressing items of income and deduction that are included in the calculation of built in gains and losses under section 382 of the internal revenue code.

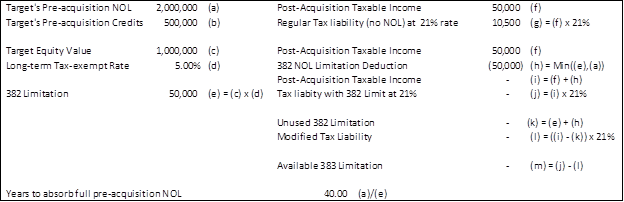

Ownership occurs when there is a shift in the owners or in the equity structure exceeding ownership rights of 50. In the event of an ownership change use of the loss corporation s nols and certain built in losses is limited to the value of the loss corporation multiplied by the adjusted federal long term. The loss corporation owned by one or more 5 percent shareholders has increased by more than 50 percentage points over the lowest percentage of stock of the loss corporation owned by such shareholders at any time during the relevant testing.

The regulations under 382 do not provide any specific guidance. In an effort to limit loss trafficking congress enacted sec.

Credits And Nols Under Section 382

Internships Are One Of The Most Important Part Of Post Graduate Diploma In Management The Students Not Only Get Diploma Courses Online College Degrees Diploma

Pch Lotto Games Power Prize Lotto Winning Numbers Win For Life Instant Win Sweepstakes

Final Regs Issued On Sec 382 Ownership Changes

Addressing Proposed Section 382 Regulations In Current M A Transactions Tax Executive

For The Record Newsletter From Andersen Q3 2019 Newsletter Sweetening The Deal The Value Of Research Tax Credits In A Merger Or Acquisition

Sec 382 Ownership And Fluctuation In Value

Https Www Csob Cz Portal Documents 10710 460146 Csob Prezentace Vysledku 4q2018 En Pdf

M A Tax For 2019

Qatar Qatar Detailed Assessment Report On Anti Money Laundering And Combating The Financing Of Terrorism

Https Www Trz Cz Upload 1 Files Ms Ar 2018 Pdf

Effective Nol Planning In Light Of Tax Reform Tax Executive

Favorable Safe Harbor Rule In Jeopardy Under Proposed Section 382 Regulations 2019 Articles Resources Cla Cliftonlarsonallen