Irc Section 672 C

The 2019 Amendments To The Delaware Trust Act Ppt Download

Inheritors Goals Control Tax Savings Ppt Download

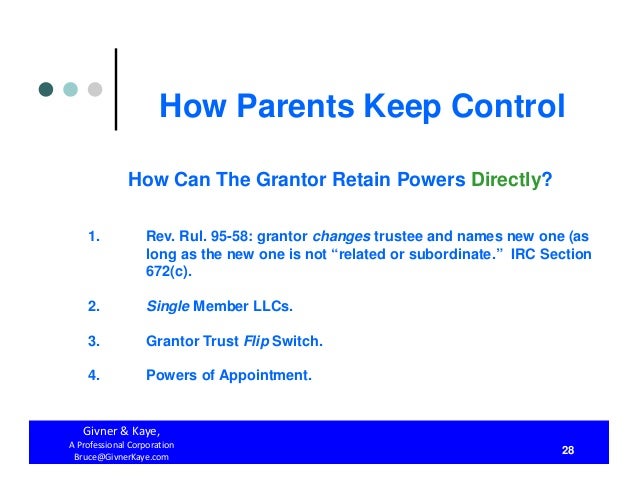

How Parents Keep Control Both During Their Lifetimes And After They A

Ilits Idgts Grats And Other Four Letter Words Ppt Download

Http Media Straffordpub Com Products Selecting Trustees And Structuring Trustee Powers Guidance For Estate Planners On Tax And Non Tax Consequences 2015 12 03 Presentation Pdf

Https Www Irs Gov Pub Irs Wd 0901030 Pdf

The grantor s father mother issue brother or sister.

Irc section 672 c. As you right imagine the definition is a bit complicated. A father or mother. The term as used in sections 674 c and 675 3 means any nonadverse party who is the grantor s spouse if living with the grantor.

But generally naming the following people can be problematic. The term related or subordinate is defined in section 672 c of the tax code. Internal revenue code 672.

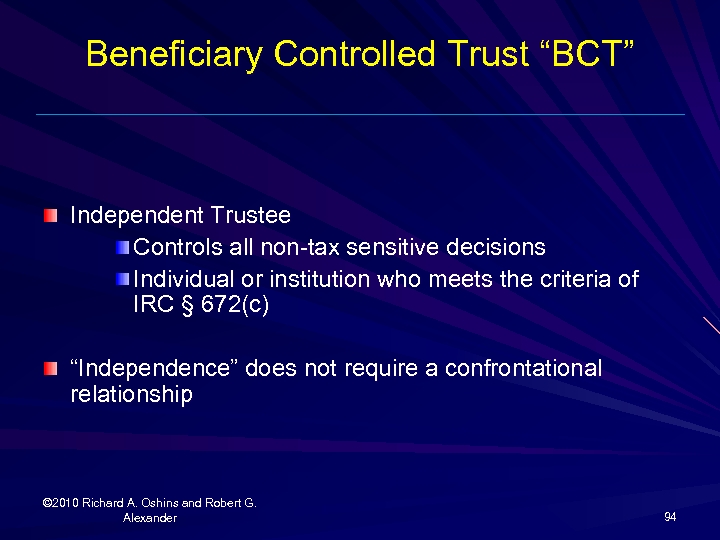

104 188 set out as a note under section 643 of this title. Or a subordinate employee of a corporation in which. An independent trustee is typically an individual or corporate entity who is not a beneficiary under the trust agreement and is not related or subordinate to the grantor his or her spouse or any of the grantor s descendants within the meaning of 26 u s.

A person shall be considered to have a power described in this subpart even though the exercise of the power is subject to a precedent giving of notice or takes effect only on the expiration of a certain period after the exercise of the power. A corporation or any employee of a corporation in which the stock holdings of the grantor and the trust are significant from the viewpoint of voting control. Section 672 c defines the term related or subordinate party.

672 u s. A brother or sister. What does it mean to be related or subordinate.

An employee of the grantor. Code unannotated title 26. A child grandchild great grandchild etc.

Https Www Kkwc Com Wp Content Uploads 2015 04 Uf Nongrantor Pdf

Pop Quiz Is This A Grantor Trust

What S An Independent Trustee Estateography

3 14 1 Imf Notice Review Internal Revenue Service

2012 Advanced Sales Forum Presented By Julius H Giarmarco J D Ll M Giarmarco Mullins Horton P C 101 W Big Beaver Road 10 Th Floor Troy Michigan Ppt Download

Https Www Dorsey Com Media Files Newsresources Publications 2014 11 A Review Of Grantor Trusts 2014fall5 Walter Impert

Welcome To The Financial And Estate Planning Council

Http Www Hallidayfinancial Com Wp Content Uploads 2019 09 July Trust Connection Pdf

Http Www Naepcjournal Org Wp Content Uploads Issue33d Pdf

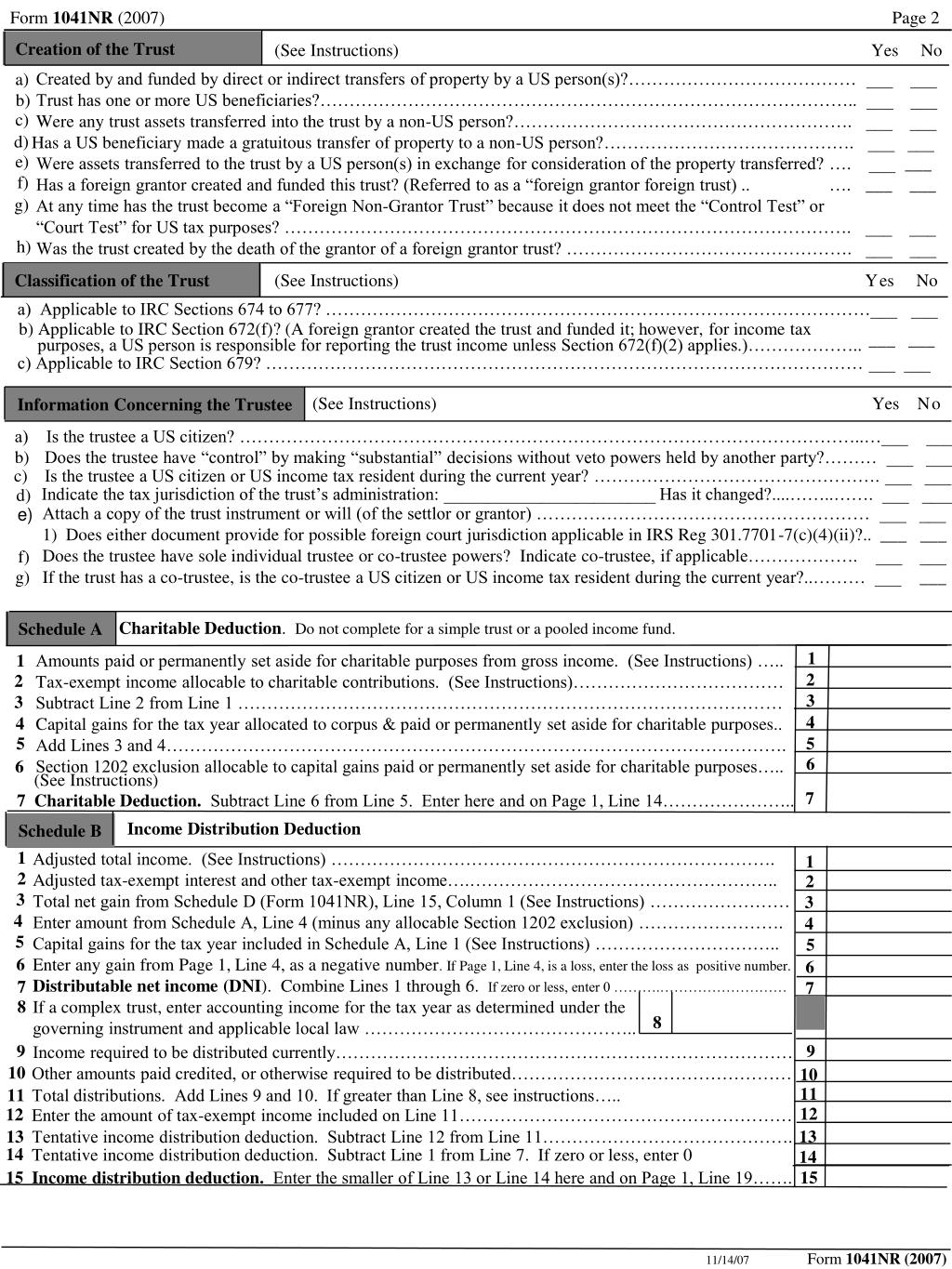

Ppt Form 1041 Nr Us Income Tax Return For Foreign Estates Trusts 2007 Omb No Powerpoint Presentation Id 6811743

The Grantor Trust Rules