Irs Section 121 Exclusion

What Is The Section 121 Exclusion Youtube

Planning Opportunities With The Sec 121 Partial Exclusion

Divorce And The Section 121 Personal Residence Exclusion Cpa Practice Advisor

1040 Sale Of Primary Residence Used As Rental

Capital Gains On Sale Of A Home The Official Blog Of Taxslayer

Home Sale Gain Exclusion Rules Under Section 121 How Does The Primary Residence Tax Exemption Work

Homeowners who have resided in their residence for at least two of the last five years may be eligible for the principal residence exclusion allowed under section 121 of the internal revenue code.

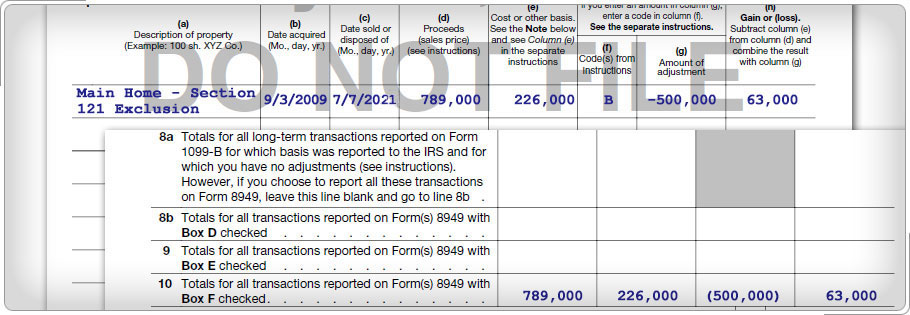

Irs section 121 exclusion. Section 121 in general section 121 of the code allows an individual to exclude up to 250 000 of gain upon the sale of a home that was owned and used as the individual s principal residence for. Qualifying for the exclusion in general to qualify for the section 121 exclusion you must meet both the ownership test and the use test. 121 a exclusion gross income shall not include gain from the sale or exchange of property if during the 5 year period ending on the date of the sale or exchange such property has been owned and used by the taxpayer as the taxpayer s principal residence for periods aggregating 2 years or more.

Section 121 of the internal revenue code of 1986 as amended by this section shall be applied without regard to subsection c 2 b thereof in the case of any sale or exchange of property during the 2 year period beginning on the date of the enactment of this act if the taxpayer held such property on the date of the enactment of this act and fails to meet the ownership and use requirements of subsection a thereof with respect to such property. Single taxpayers are entitled to a 250 000 exclusion and married taxpayers filing jointly are entitled to a 500 000 exclusion. 121 b limitations.

This exception is known as the home sale gain exclusion and it s found in section 121 of the internal revenue code. Now there is an exception to the general rule of paying tax on your gain when it comes to your primary residence.

Solved How Do I Obtain 121 Exclusion On Portion Of Duplex Community

Favorable Tax Rules For Military When Excluding Capital Gain From Sale Of Principal Residence Katehorrell

Publication 523 Selling Your Home Chapter 2 Rules For Sales In 2001 Reporting The Gain

Section 121 Exclusion Can Boost Reis Returns Biggerpockets Blog

Irs Courseware Link Learn Taxes

The Home Sale Gain Exclusion

Https Cdn2 Hubspot Net Hubfs 26654 Docs 2017 Principal Residence Exclusion Fs Pa Pdf

Sale Of Primary Residence Capital Gains Tax

New Law S Reduced Homesale Exclusion For Nonqualified Use Will Mean Headaches For Sellers Years Down

Publication 908 02 2020 Bankruptcy Tax Guide Internal Revenue Service

1031 Exchange And Primary Residence Asset Preservation Inc

A Trust Can Qualify For A Section 121 Deduction Pollock Firm

Understanding Section 121 The Universal Exclusion On A Home Sale