Section 92 Of Income Tax Act

The Itr 4 Form Which Also Called Sugam For Those Taxpayers Who Have Opted For The Presumptive Income Sc Income Tax Return Online Taxes Tax Return

Income Tax Audit Individual Or Business Person Has To Get His Book Of Accounts Reviewed As Per Section 44ab Of Income Tax Act 1961 Income Tax Types Of Taxes Finance

Pin On Income Tax

Pin By Karthik Shetty On India General Knowledge Facts Legal Advice Income Tax Preparation

Section 203 Of The Income Tax Act 1961 Mandates The Employer To Deduct Tds And Issue Certificates In The Forms16 Detailed About The D Certificate Type Taxact

As Per The Changed Rules Notified Under Section 234f Of The Income Tax Act Which Came Into Effect From April 1 2017 Income Tax Tax Software Income Tax Return

Clause 30 of the bill seeks to amend section 92ce of the income tax act relating to secondary adjustment in certain cases.

Section 92 of income tax act. I one enterprise holds directly or indirectly shares carrying not less than twenty six per cent of the voting power in the other enterprise. Section 92d of income tax act maintenance and keeping of information and document by persons entering into an international transaction or specified domestic transaction section 92d. When the assessee enters into a transaction in which one of the parties to the transaction is a person located in a notified jurisdictional area then all the parties to the transaction are deemed to be the associated enterprises as per section 92a of the income tax act.

Sub section 1 of the said section inter alia provides that the assessee shall make secondary adjustment in case where primary adjustment to transfer price takes place as specified therein. Comptroller means the comptroller of income tax appointed under section 3 1 and includes for all purposes of this act except the exercise of the powers conferred upon the comptroller by sections 34f 9 37ie 7 37j 5 67 1 a 95 96 96a and 101 a deputy comptroller or an assistant comptroller so appointed. The income tax department appeals to taxpayers not to respond to such e mails and not to share information relating to their credit card bank and other financial accounts.

1 any income arising from an international transaction shall be computed having regard to the arm s length price. This statutory definition is as follows. Section 92 c refers to the expression transaction which in turn is defined under section 92f v in an inclusive manner.

Substitution of new sections for section 92. 1 every person who has entered into an international transaction or specified domestic transaction shall keep and maintain such information and document in respect thereof as may be prescribed. The income tax department never asks for your pin numbers passwords or similar access information for credit cards banks or other financial accounts through e mail.

Computation of income from international transaction having regard to arm s length price. Section 92a 2 provides that two enterprises shall be deemed to be associated enterprises for the purposes of sub section 1 if at any time during the previous year. For section 92 of the income tax act the following sections shall be substituted with effect from the 1st day of april 2002 namely.

1 notwithstanding anything to the contrary contained in section 139 where any person has entered into an agreement and prior to the date of entering into the agreement any return of income has been furnished under the provisions of section 139 for any assessment year relevant to a previous year to which such agreement applies such person shall furnish within a period of three months from the end of the.

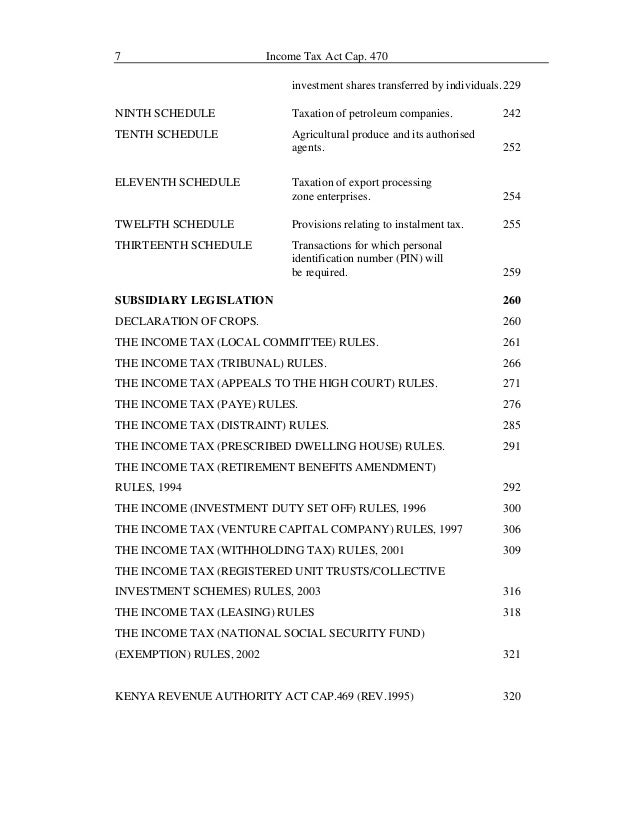

Income Tax Act Kenya

Income Tax Deduction Under Section 80u Income Tax Tax Deductions Tax

Let S Start With The Basics Of A Tax Return Online Taxes Filing Taxes File Taxes Online

Tds On Payments To Non Residents Section 195

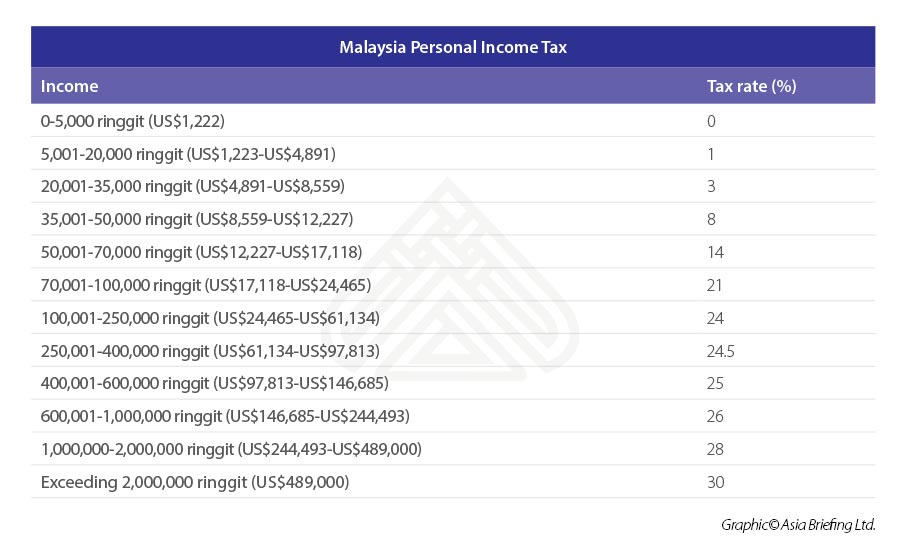

Individual Income Tax In Malaysia For Expatriates

Pin On Income Tax

House Rent Receipt Templates Receipt Of House Rent Receipt Template Template Printable Invoice Template

Penalties Under Income Tax Act 1961

New Gst Registration After Cancellation Taxreturnwala Indirect Tax Government Grants Filing Taxes

Pin On Talking Points

Deduction Under Section 80u Of The Income Tax Act 1961 Can Be Claimed By An Individual Who Is A Resident Income Tax Return Online Taxes Tax Deducted At Source

2014 Tax Season To Start Later Following Government Closure Irs Sees Heavy Demand As Operations Resume Taxes Humor Tax Preparation Make Money Now

Highlights To The Financial Deadlines In The Coming Year 2019 Online Taxes Filing Taxes File Taxes Online