Nongovernmental Section 457 Plan

Ultimate Guide To Non Governmental 457 B Plans

8 Questions Plan Sponsors Should Ask About 457 B And 457 F Plans Strategic Benefit Services

W2 Tax Return Google Sok

Should I Invest In My 457 The What Why And When With Images Investing Deferred Compensation Retirement Fund

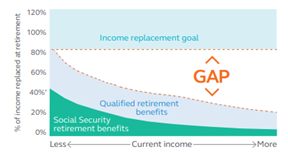

Should You Use Your 457 B Investing Personal Finance White Coat Investor

An Overview Of Restricted Stock Units In A Nonqualified Deferred Compensation Plan Executive Benefit Solutions

Comparison of tax exempt 457 b plans and governmental 457 b plans.

Nongovernmental section 457 plan. They allow you to defer your salary during peak income years but have distinct distribution options compared to qualified plans such as 401k and 403b. Benefits of a 457 b plan 1 additional savings. 2 no early withdrawal penalty.

In general under a 457 b plan which is also referred to as an eligible deferred compensation plan a participant may defer amounts of compensation and income earned on those deferrals and avoid federal income taxation until those amounts are paid to the participant. The main benefit of using a 457b plan is you basically get another 401k 403b. You can double your tax deduction and double your savings.

The employer provides the plan and the employee defers compensation into it on a pre tax or after tax roth basis. They can be either eligible plans under irc 457 b or ineligible plans under irc 457 f. Nongovernmental 457 b plans addressed below are available only to a select group of management or highly compensated employees of tax exempt nonprofit corporations such as hospitals.

For the most part the plan operates similarly to a 401 k or 403 b plan with which most people in the us are familiar. A 457 plan is among the most complex of employer sponsored plans. A 457 plan sponsor must be either.

Definition and purpose of the non governmental 457 plan a non governmental 457 plan is defined as an extra or bonus tax advantaged salary deferral plan for a select group of employees. The 457 plan is a type of nonqualified tax advantaged deferred compensation retirement plan that is available for governmental and certain nongovernmental employers in the united states. Generally speaking 457 plans are non qualified tax advantaged deferred compensation retirement plans offered by state governments local governments and some nonprofit employers.

If you are a state or local government employee or an employee of a 501 c tax exempt non profit you may have a 457 plan. Internal revenue code section 457 provides tax advantaged treatment for certain non qualified deferred compensation plans. Plans of deferred compensation described in irc section 457 are available for certain state and local governments and non governmental entities tax exempt under irc section 501.

What Is A 457 Deferred Compensation Plan

403 B Plans And 457 B Plans Retirement Plan The Ryding Company

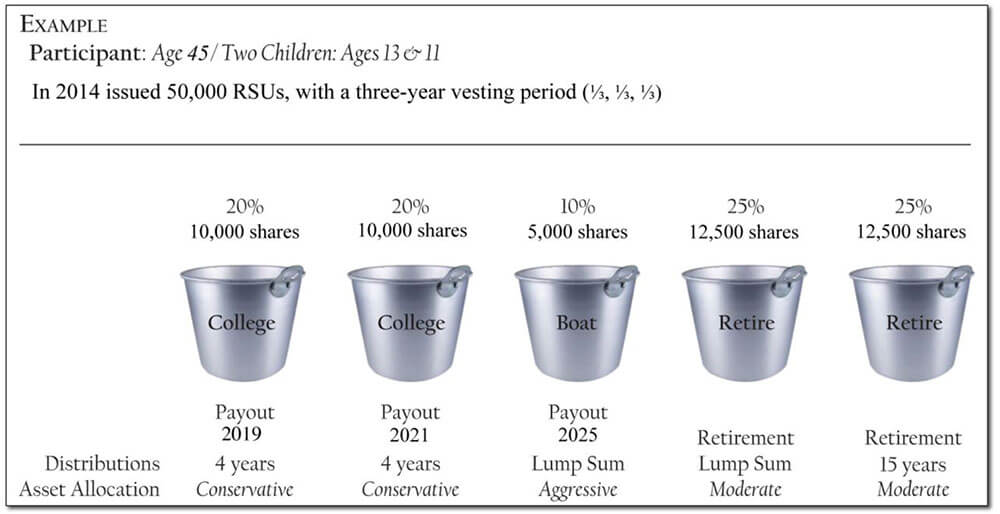

Superfunding Retirement With The Special 457 Plan Three Year Catch Up

Moving The Goalposts Attack Of The Lifestyle Creep Personal Finance Finance Investing

Nonqualified 457 Plans Strengthen Your Organization And Drive Key Employee Performance Presenter S Name The Presenter S Title Goes On This Line Nonqualified Ppt Download

Is A 457 Plan Right For You Butterfield Schechter Llp

Know The Pros And Cons Of Your 457 Mar 23 2000

Understanding The 457 B Market National Association Of Plan Advisors

A Checklist For Drafting Section 457 F Plans For Tax Exempt Employers

A Review Of Providence S 457 B Plan Above The Canopy

:max_bytes(150000):strip_icc()/401k-investing-success-tips-56a090ef5f9b58eba4b19e9c.jpg)

457 Plan Definition

457 Plans Butterfield Schechter Llp

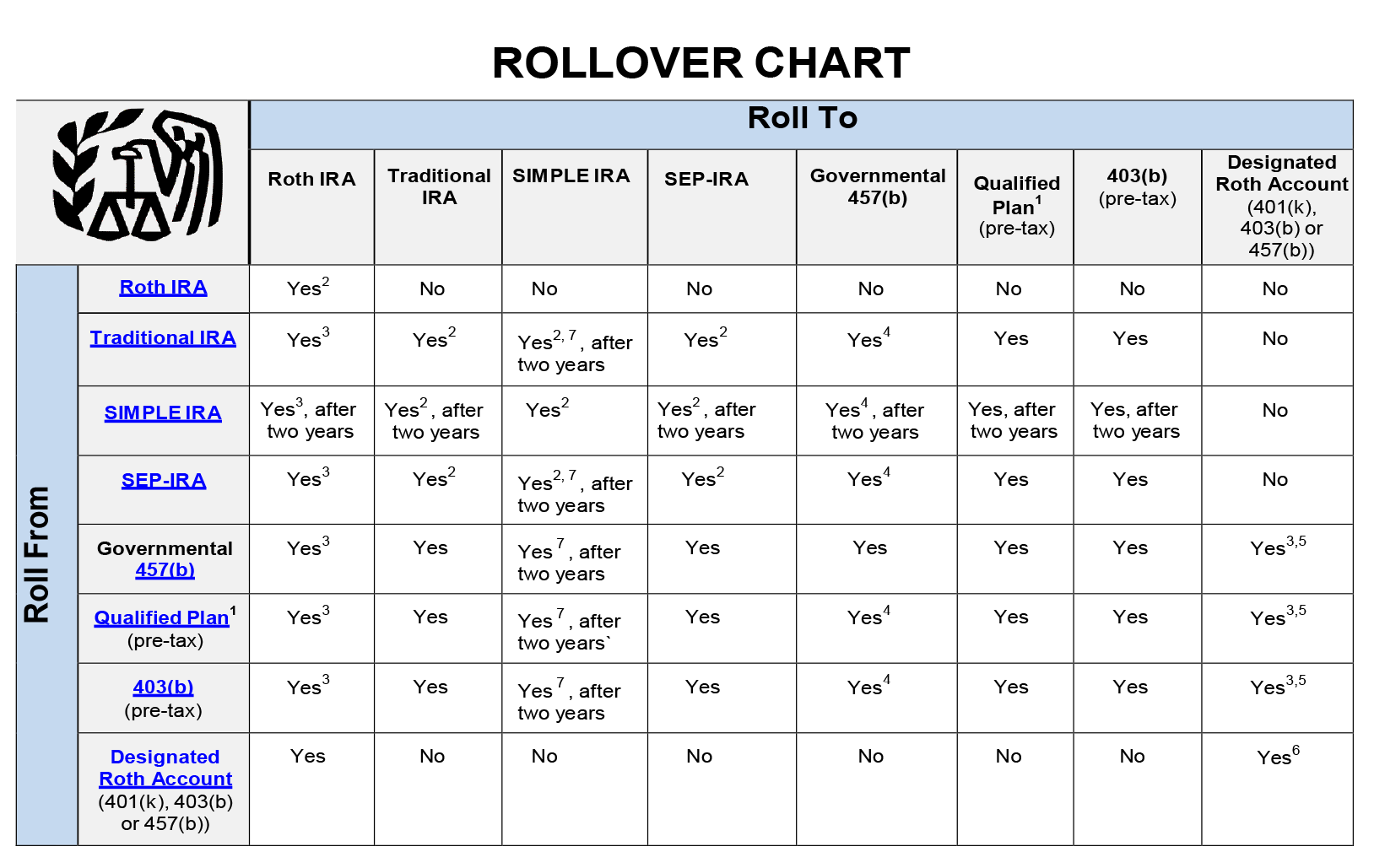

Rolling Over Funds From One Retirement Account To Another National Benefit Services