Section 153 Of Income Tax Act

What Is The Time Limit For Completion Of Assessments Types Of Taxes Allowance Saving

Companies Appointment And Qualification Of Directors Amendment Rules 2017 Http Taxguru In Company Law Companies Appo With Images Qualifications Appointments Company

Axbracket Proposal2018newversion Tax Brackets Tax Rules Income Tax Brackets

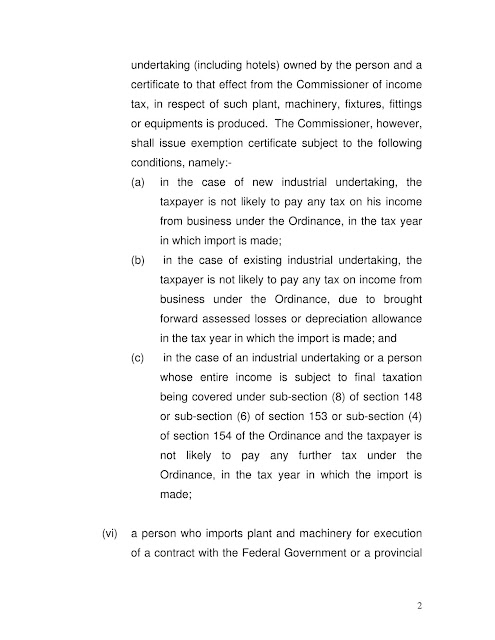

How To Obtain Exemptions Under Various Provsions Of Income Tax Ordinance 2001 Sample Letters Included

Bloomington Future Debt And Interest Debt Bloomington Financial Statement

Http Download1 Fbr Gov Pk Sros 2019101151017301sro1160 Pdf

B for the rendering of or providing of services.

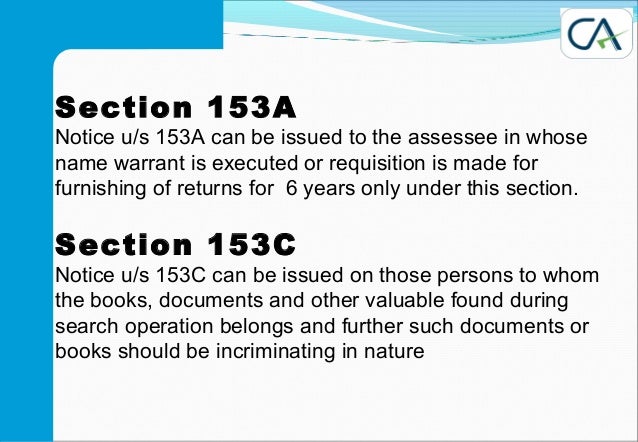

Section 153 of income tax act. 153 1 every person paying at any time in a taxation year a salary wages or other remuneration other than i amounts described in subsection 212 5 1 and ii amounts paid at any time by an employer to an employee if at that time the employer is a qualifying non resident employer and the employee is a qualifying non resident employee. Enforceability of section 153a section 153c an analysis. 3 the provisions.

Time limit for completion of assessment reassessment and recomputation 1 no order of assessment shall be made under section 143 or section 144 at any time after the expiry of twenty one months from the end of the assessment year in which the income was first assessable. Substituted by the direct tax laws amendment act 1987 w. Substituted by the finance act 1989 w.

The income tax department appeals to taxpayers not to respond to such e mails and not to share information relating to their credit card bank and other financial accounts. Section 153 3 in the income tax act 1995 3 the provisions of sub sections 1 and 2 shall not apply to the following classes of assessments reassessments and recomputations which may 5 subject to the provisions of sub section 2a be completed at any time. Section 153 in the income tax act 1995 1.

Section 153c of the act relates to assessment of income of any other person. For section 153 of the income tax act the following section shall be substituted with effect from the 1st day of june 2016 namely. The income tax department never asks for your pin numbers passwords or similar access information for credit cards banks or other financial accounts through e mail.

Section 153 a of the income tax act 1961 provides for the scheme of assessment of income in case of a searched person. The income tax ordinance 2001 section. 1 no order of assessment shall be made under section 143 or section 144 at any time after the expiry of twenty one months from the end of the assessment year in which the income was first assessable.

Prior to the substitution sub. Prior to the substitution subsection 1 as amended by.

If You Are Facing A Problems In Making Your Tax Related Work And Not Able To Complete It Alone Or Need So Free Tax Filing Tax Preparation Services Filing Taxes

Pin By Martin Campbell On Political Cartoons Medicaid Political Cartoons Medicare

Search And Seizure2014

Oecd Ilibrary Home

Notice U S 143 2 For Scrutiny U S 143 2 Tax2win

Understanding Provisions Of Withholding Taxes Under The Income Tax Ordinance 2001

Censor Board Denied Certificate To 793 Films In 16 Yearspic Twitter Com Ee1bypjtrg Censored Denied Twitter Com

Section 140a Self Assessment Of Income

Pin By Corpbiz Advisors On Corpbiz In 2020 Investors Investments Options Financial Investments

From Thurman Malik I Wish You A Prosperous Year In 2017 I Have Started Filing Taxes Early This Year Let S Talk About Your Filing Taxes Tax Refund Tax Prep

Should We Terminate The Coverdell Education Savings Account Education Savings Account Accounting Saving For College

Bloomington Future Debt And Interest Debt Bloomington Financial Statement

Incarceration Rate Prison Reform