Section 481 Adjustment Example

The Top Heavy Update Pages With Too Many Ads Above The Fold Now Penalized By Google S Page Layout Algorithm Page Layout Ads Banner Online

Event Proposal Templates 14 Free Printable Word Pdf Formats Event Proposal Template Event Proposal Proposal Templates

Https Tax Thomsonreuters Com Site Wp Content Pdf Checkpoint Handbook Updates Checkpoint Specialreport Tp3115 Pdf

Https Www Calt Iastate Edu System Files Premium Video Files Form 20 203115 20part 201 Pdf

Credit Karma Offers Free Weekly Credit Reports And Monitoring Credit Karma Credit Card App Good Credit

4 10 8 Report Writing Internal Revenue Service

Section 481 a adjustments.

Section 481 adjustment example. You report 4 000 of gain on the sale of the shares and in addition you have a 2 000 section 481 a adjustment. At the end of 2004 you held shares with 24 000 basis but value of 26 000. Neither the company nor any of its subsidiaries has elected or agreed or is required to make any adjustment under section 481 a of the code by reason of a change in accounting method or otherwise that would result in taxable income in any taxable period after the closing date.

You made the mark to market election effective beginning in 2005 and ended up selling these shares for 30 000. A section 481 a loss is deductible in full. The company earned 300k in december of the cash basis year which they received in january of the accrual basis year.

Section 481 provides that where a taxpayer s taxable income for a tax year is computed under a method of accounting different from that previously used an adjustment will be made to prevent amounts from being duplicated or omitted solely by reason of the change in accounting method. 1954 is a taxable year beginning after december 31 1953 and ending. Sample 1 section 481 a adjustments.

The amendments made by this section amending this section and section 381 of this title shall apply with respect to any change in a method of accounting where the year of the change within the meaning of section 481 of the internal revenue code of 1986 formerly i r c. A cash basis taxpayer switches to accrual basis.

1 Form 3115 Line By Line All Audio Is Streamed Through Your Computer Speakers There Will Be Several Attendance Verification Questions During The Live Ppt Download

No Stone Left Unturned A Methods Based Analysis Of The Cares Act And Opportunities To Utilize Its Provisions Eversheds Sutherland

E5f3a978d73aed27de3f80bb5632832a Jpg 325 481 Knots Diy Macrame Knots Knots

Neu Lebenslauf Vorlage 2016 Kostenlos Briefprobe Briefformat Briefvorlage Lebenslauf Vorlagen Word Briefvorlagen Lebenslauf

Tumblr Sajt

Unicap Changing To The Modified Simplified Production Method

Professional Resume Template 2 Page Resume 1 Page Cover Letter Professional Template Microsoft Word Resume Cv Design Resume Template Professional Resume Templates Resume Template

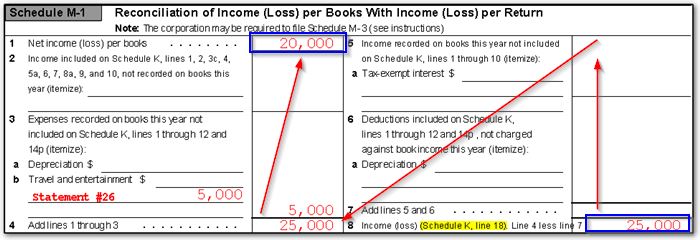

1120s Calculating Book Income Schedule M 1 And M 3 K1 M1 M3

25 Best Resume Templates With Cover Letter Modern Resume Design Modern Resume Template Best Resume Template

Mad Magazine In The 60 S Had One Of The Greatest Caricaturists In Mort Drucker Star Blecch 02 Comic Artist Mad Magazine Comic Books

Dorm Room Checklist Png 481 933 Pixels Dorm Room Checklist College Dorm College Room

Pin By Samia Maamouri On Broderie In 2020 Quilting Stitch Patterns Free Motion Quilt Designs Machine Quilting Patterns

New Brand Identity For Madeleine Blanchfield Architects Bp O Business Cards Creative Debossed Business Card Business Card Design