Section 105 Irs

Using A Section 105 Medical Reimbursement Plan To Reduce Your Tax Bill Above The Canopy

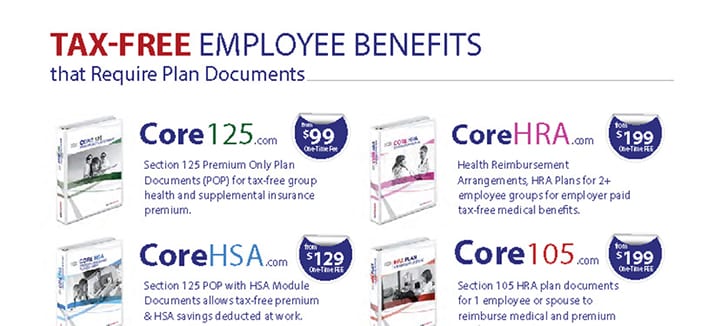

Section 105 Plan Explained Core Documents

A Small Business Owner S Guide To Section 105 Plans

Section 105 Plans How To Save Taxes If You Own A Microbusiness

Section 105 Companies Act 2016 Fill Online Printable Fillable Blank Pdffiller

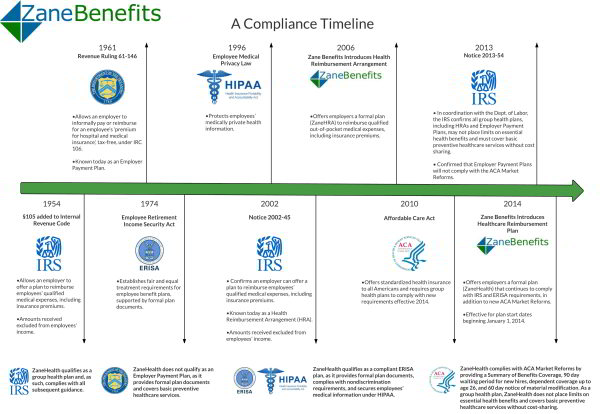

Compliance Nuesynergy

They will advise the type of section 105 plan self insured qsehra stand alone reimbursement plans or group integrated hra plan to choose that best fits with the business legal structure.

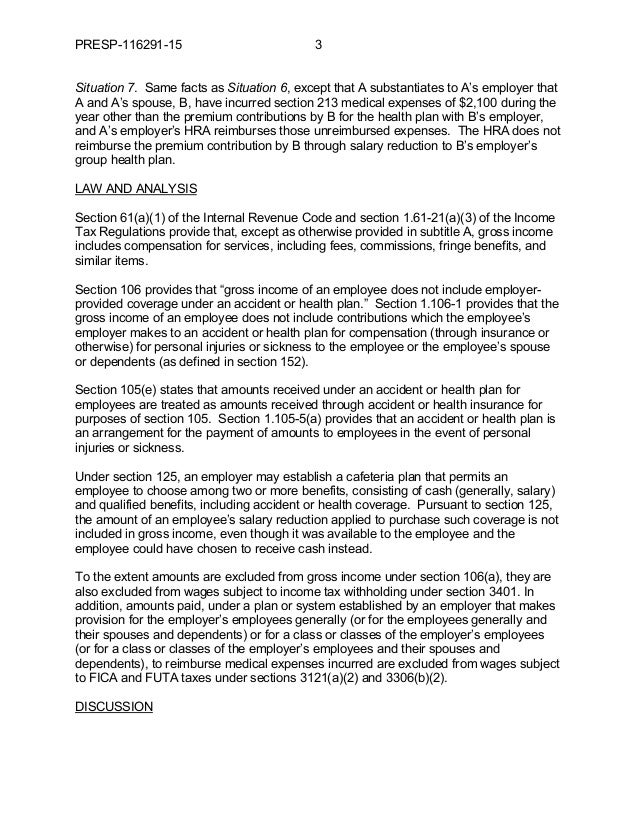

Section 105 irs. Section 105 sets the following requirements for an eligible plan. Section 105 plans are used by employers in a variety of ways. For purposes of this section and section 104 1 amounts received under an accident or health plan for employees and 2 amounts received from a sickness and disability fund for employees maintained under the law of a state or the district of columbia shall be treated as amounts received through accident or health insurance.

A section 105 plan is an irs regulated health benefit that allows the tax free reimbursement of medical and insurance expenses as described under section 105 of the internal revenue code irc. 1954 or under section 505 d of the tax reform act of 1976 set out below as such sections were in effect before the enactment of this act may 23 1977 for a taxable year beginning in 1976 if such election is not revoked under subsection c of this section set out above and. For some business owners this can be a savings of thousands of dollars per year.

With a section 105 plan you can deduct your entire family s medical expenses with without being subject to the 10 agi floor. Irc section 105 is the section of irs tax code that discusses amounts received under accident and health plans. Irc section 105 allows qualified distributions from accident and health plans to be excluded from income tax free.

Irs section 105 addresses the exclusion of reimbursements provided by an accident or health plan for the medical expenses of an individual or their dependents from the individual s gross taxable income. Next the business owner should choose a start date for the plan. On september 30 2019 the irs and the department of the treasury issued proposed regulations clarifying the application of the employer shared responsibility provisions in code section 4980h and the nondiscrimination rules in code section 105 h to individual coverage hras and providing proposed safe harbors for the application of those provisions to individual coverage hras with certain changes compared to the potential safe harbors described in notice 2018 88.

Employers are the sole contributors to the plan. Section 105 a provides that amounts received by an employee through accident or health insurance for personal injuries or sickness are included in gross income to the extent such amounts 1 are attributable to contributions by the employer that were not includible in the gross income of the employee or 2 are paid by the employer. Even better it s a deduction from income tax at the state and federal levels and a deduction from payroll taxes.

What Is A Section 105 Plan Or Hra How To Set One Up

The History Of Health Insurance Reimbursement

What Is The Health Insurance Deduction For A Sole Proprietor Core Documents

Answers To The Top 4 Questions About Section 105 H Nondiscrimination Testing

Section 105 Plans Zane Benefits Publishes New Intel Zane Benefits Inc

Clearpath Benefit Advisors Employee Benefits Columbus Ohio Section 105 H Nondiscrimination Testing

Merp Guidelines Irs Ruling Notice Dtd 10 2015

Health Reimbursement Arrangements Explained Hra Plan Document 99core Documents

Compare 2020 Hra Options With This Handy Tool From Core Documents Core Documents

Nondiscrimination Rules Summary Of Irc 105 H Eligibility And Benefits Rules Leavitt Group News Publications

Enhanced Health Benefits For Executives That S Another Affordable Care Act Issue To Consider The Retirement Plan Blog

Fixed Indemnity Sick Pay Taxable In Cafeteria Plans Irs Memo Core Documents

Form 105 Mvat Filled Sample Fill Online Printable Fillable Blank Pdffiller