Section 125 Nondiscrimination Rules

Cafeteria Plan Nondiscrimination Tests Abd Insurance Financial Services

Irs Issues New Proposed Cafeteria Plan Regulations Kibble And

Http Amben Com Demos Nondiscriminationtesting Abg Nondiscriminationtestingguide Pdf

Understanding Section 125 Cafeteria Plans

Hsa Nondiscrimination Rules Abd Insurance Financial Services

Https Www Dms Myflorida Com Content Download 140605 907025 Cafeteria Plan 2018 Pdf

To satisfy the section 125 nondiscrimination.

Section 125 nondiscrimination rules. If you also offer health flexible spending account fsa or dependent care fsa benefits there are additional tests to complete. Plans that are offered under a cafeteria plan which is generally the case must also pass section 125 nondiscrimination testing which determines whether the salary reductions for coverage under these. Section 13304 of p l.

The irs imposes nondiscrimination rules on section 125 plans also known as flexible benefit plans cafeteria plans or pre tax premium plans and self funded group health plans. If a cafeteria plan is discriminatory highly compensated employees health plan contributions will be taxable. In order to operate a plan that offers eligible benefits on a pre tax basis.

These rules only affect whether reimbursements made under the plan are taxable. Because code section 125 cafeteria plans and the component benefits within the 125 plan enjoy favorable tax treatment the code s nondiscrimination rules exist to prevent plans from being designed in such way that it discriminates in favor of individuals who are either highly compensated employees hce or are otherwise key employees key in. Cafeteria plans are generally subject to the nondiscrimination requirements of internal revenue code section 125.

All of the possible tests are listed below. Although the section 105 h rules do not apply to an employer s fully insured group health plan the section 125 nondiscrimination rules will apply if the health plan is offered through a cafeteria plan. A general transitional rule any cafeteria plan in existence on february 10 1984 which failed as of such date and continued to fail thereafter to satisfy the rules relating to section 125 under proposed treasury regulations and any benefit offered under such a cafeteria plan which failed as of such date and continued to fail thereafter to satisfy the rules of section 105 106 120.

For amounts incurred or paid after 2017 the 50 limit on deductions for food or beverage expenses also applies to food or beverage expenses excludable from employee income as a. If you sponsor a cafeteria section 125 plan there are three tests to complete. Wages and at least one nontaxable benefit e g.

Self insured medical reimbursement plans that are offered under a cafeteria plan which is generally the case must also pass section 105 h nondiscrimination testing which determines whether reimbursements made under the plan are taxable. Nondiscrimination rules generally a section 125 plan commonly referred to as a cafeteria plan is a plan that offers employees a choice between at least one permitted taxable benefit e g. The purpose of the rules is to prevent employers from favoring highly compensated employees to an impermissible degree.

Exhibit104

Pin On Mental Health

Http Www Sourcemediaconferences Com Bfe09 Pdf Joyner Pdf

Section 125 Administration

The Counting By 1 S A Math Worksheet From The Halloween Math Worksheets Page At Math Drills Com Halloween Math Worksheets Halloween Math Math Worksheets

امتحان تجريبي في اللغة العربية للصف الثامن الفصل الدراسي الاول 2016 ـ 2017 مدونة تعلم Make Real Money Chemistry Free Music Worksheets

Group Dynamic Inc Compliance Services

The Counting By 1 S A Math Worksheet From The Halloween Math Worksheets Page At Math Drills Com Halloween Math Worksheets Halloween Math Math Worksheets

Sba Paycheck Protection Program Faqs

Https Www Bidnet Com Bneattachments 527534797 Pdf

Https Www Ebcflex Com Portals 8 Pdf Keeping Up Design Options And Testing Wp Pdf

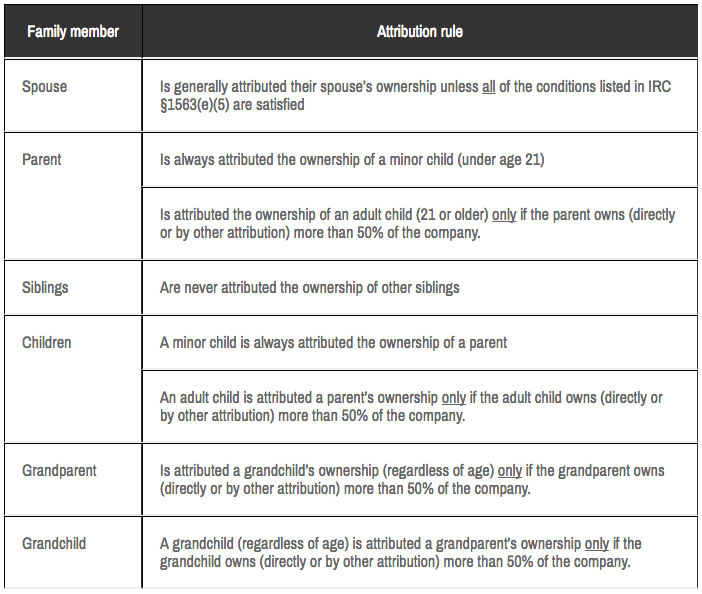

Is Your Company Part Of A Controlled Group You Need To Know Or Risk 401 K Plan Disqualification

Hr Service Inc Making Hr Outsourcing And Compliance Simple

/GettyImages-1133007677-22b35aad9da34a55989626cf40b8a456.jpg)