Section 179 Election

Expense Election Irs Code Section 179 Where Are We Going And Where Have We Been Farmdoc Daily

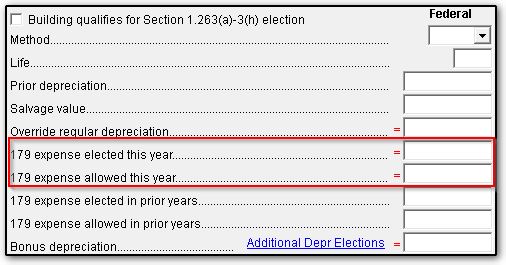

4562 Section 179 Data Entry

S Corps Should Beware How Elections Are Made Shindelrock

2020 Section 179 Tax Benefit For Business Envision Capital Group

The Section 179 And Section 168 K Expensing Allowances Current Law And Economic Effects Everycrsreport Com

Standard Mileage Deduction Vs Section 179 For Rideshare Drivers

First there is a dollar limitation.

Section 179 election. The form used to report information for a section 179 deduction is irs form 4562 which collects information on business property acquired and put into service. The amended return must be filed within the time prescribed by law. The section 179 election is subject to three important limitations.

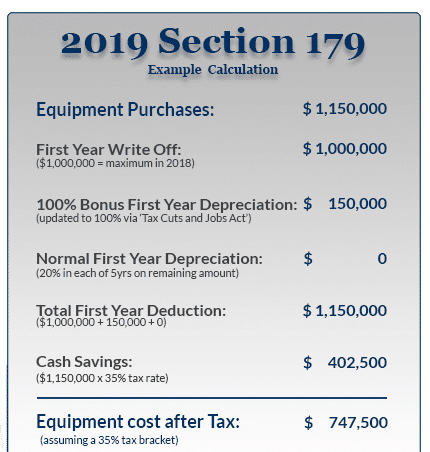

Specify the items of section 179 property to which the election applies and the portion of the cost of each of such items which is to be taken into account under subsection a and b be made on the taxpayer s return of the tax imposed by this chapter for the taxable year. The 2020 section 179 deduction limit for businesses is 1 040 000 jan 16 2020 the section 179 deduction for 2020 is 1 040 000 dollars. Section 179 does come with limits there are caps to the total amount written off 1 040 000 for 2020 and limits to the total amount of the equipment purchased 2 590 000 in 2020.

The phase out limit increased from 2 million to 2 5 million. An election or any specification made in the election to take a section 179 deduction for 2019 can be revoked without irs approval by filing an amended return. 179 c 1 b be made on the taxpayer s return of the tax imposed by this chapter for the taxable year.

Once made the revocation is. The dollar amount is adjusted each year for inflation. The total amount you can take as section 179 deductions for most property including vehicles placed in service in a specific year can t be more than 1 million.

You can use it to claim a depreciation deduction make a section 179 election and take a bonus depreciation deduction. Companies can deduct the full price of qualified equipment purchases up to 1 040 000 with a total equipment. For tax years beginning after 2017 the tcja increased the maximum section 179 expense deduction from 500 000 to 1 million.

Under section 179 b 1 the maximum deduction a taxpayer may elect to take in a year is 1 000 000 as of january 1 2018. The amended return must also include any resulting adjustments to taxable income. Specify the items of section 179 property to which the election applies and the portion of the cost of each of such items which is to be taken into account under subsection a and i r c.

Section 179 Depreciation Tax Deduction 2016 2019 Taycor Financial 2016 02

Section 179 Deduction And Bonus Depreciation Requirements Olsen Thielen Certified Public Accountants Consultants

Depreciation And The Tcja Strategic Finance

4562 Listed Property Type 4562

Controlled Groups And The Sec 179 Election For S Corporations

2018 Irs Section 179 Deduction News Update For Businesses

Form 4562 A Simple Guide To The Irs Depreciation Form Bench Accounting

Https Resources Taxschool Illinois Edu Taxbookarchive 2011 2011b 2004 20depreciation Pdf

The Economic Stimulus Act Of 2008

Section 179 Depreciation Income Tax Course Tcja 2017 Cpa Exam Regulation Tax Cuts 2017 Youtube

Understanding Asset Depreciation Section 179 Deductions Paychex

How Section 179 Tax Deductions Can Save A Small Business Money In Ca

Depreciation Refresher 2017