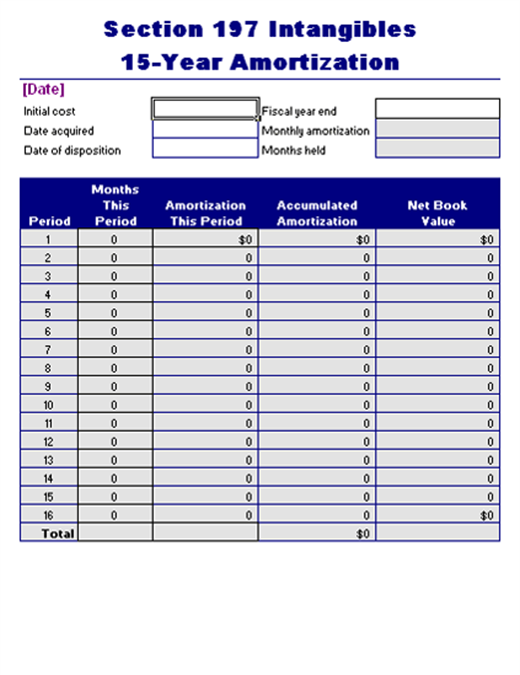

Section 197 Amortization

Http Www Kirkland Com Sitefiles Kirkexp Publications 2582 Document1 Transactional 20guide 20to 20new 20code 20section 20197 Pdf

Intangible Asset Depreciation

Budget E Pil A Confronto Infografiche Per Conoscere Il Budget Dell Ue Budgeting Infographic

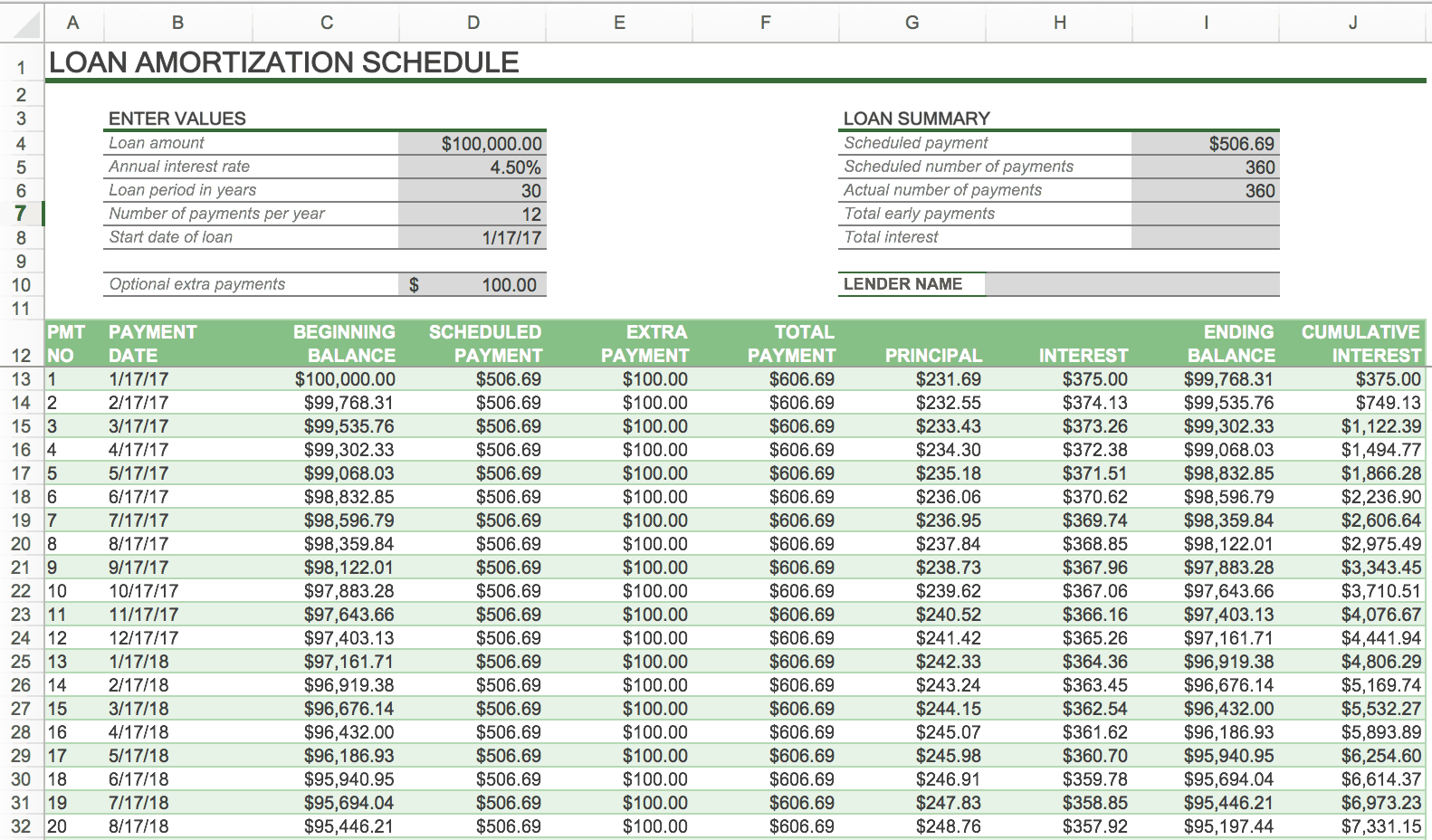

How To Create An Amortization Schedule Smartsheet

Pin On Work

Account Registration Design Pattern Example At Myspace 2 Of 197

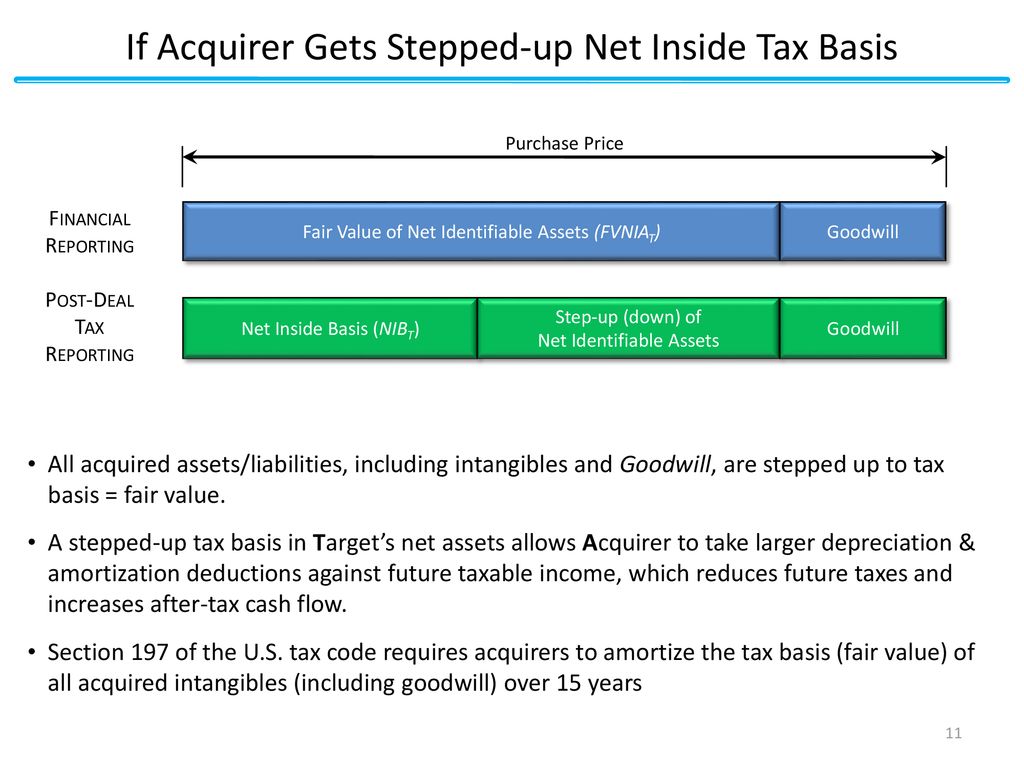

A taxpayer shall be entitled to an amortization deduction with respect to any amortizable section 197 intangible.

Section 197 amortization. The amount of such deduction shall be determined by amortizing the adjusted basis for purposes of determining gain of such intangible ratably over the 15 year period beginning with the month in which such intangible was acquired. The amount of such deduction shall be determined by amortizing the adjusted basis for purposes of determining gain of such intangible ratably over the 15 year period beginning with the month in which such intangible was acquired. The irs designates certain assets as intangible assets under section 197 of the internal revenue code.

The amount of such deduction shall be determined by amortizing the adjusted basis for purposes of determining gain of such intangible ratably over the 15 year period beginning with the month in which such intangible was acquired. Cost attributable to other property. Section 197 amortization rules apply to some business assets but not to others.

8 treatment of certain increments in value. You must amortize these costs if you hold the section 197 intangibles in connection with your trade or business or in an activity engaged in for the production of income. A taxpayer shall be entitled to an amortization deduction with respect to any amortizable section 197 intangible.

These intangible assets must usually be amortized over 15 years.

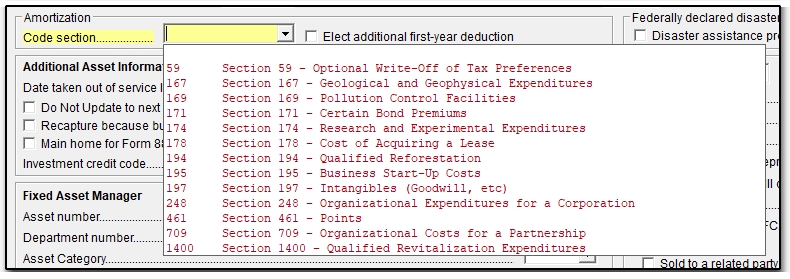

10266 4562 Entering Amortized Assets

First Of Many 1 6kw Solar Tile Pv Systems Installed Onto New Build Homes For A Developer In Mansfield Nottinghamshire Visit Solar Tiles Pv System Solar Pv

Understanding Tax Amortization Benefit Considerations And The International Impact Valuation Research

Amortization Of Legal Fees Intuit Accountants Community

Ex 99 2 3 A16 16168 1ex99d2 Htm Ex 99 2 Exhibit 99 2 Supplemental Financial Information Second Quarter 2016 Graphic Table Of Contents Second Quarter 2016 Forward Looking Statements 3 Consolidated Balance Sheets 4 5 6 7 8 9 10 11 12

Goodwill Differences Between Gaap And Tax Accounting Wall Street Prep

Dribbble Real Pixels Jpg By Aykut Yilmaz In 2020 Infographic Layout Templates Brochure Template Layout Corporate Brochure Design

Icahn Enterprises L P 2020 Current Report 8 K

Https Www Thompsonhine Com Uploads 1136 Doc Domestic Taxable Mergers And Acquisitions Pdf

Property Acquisition And Cost Recovery Ppt Video Online Download

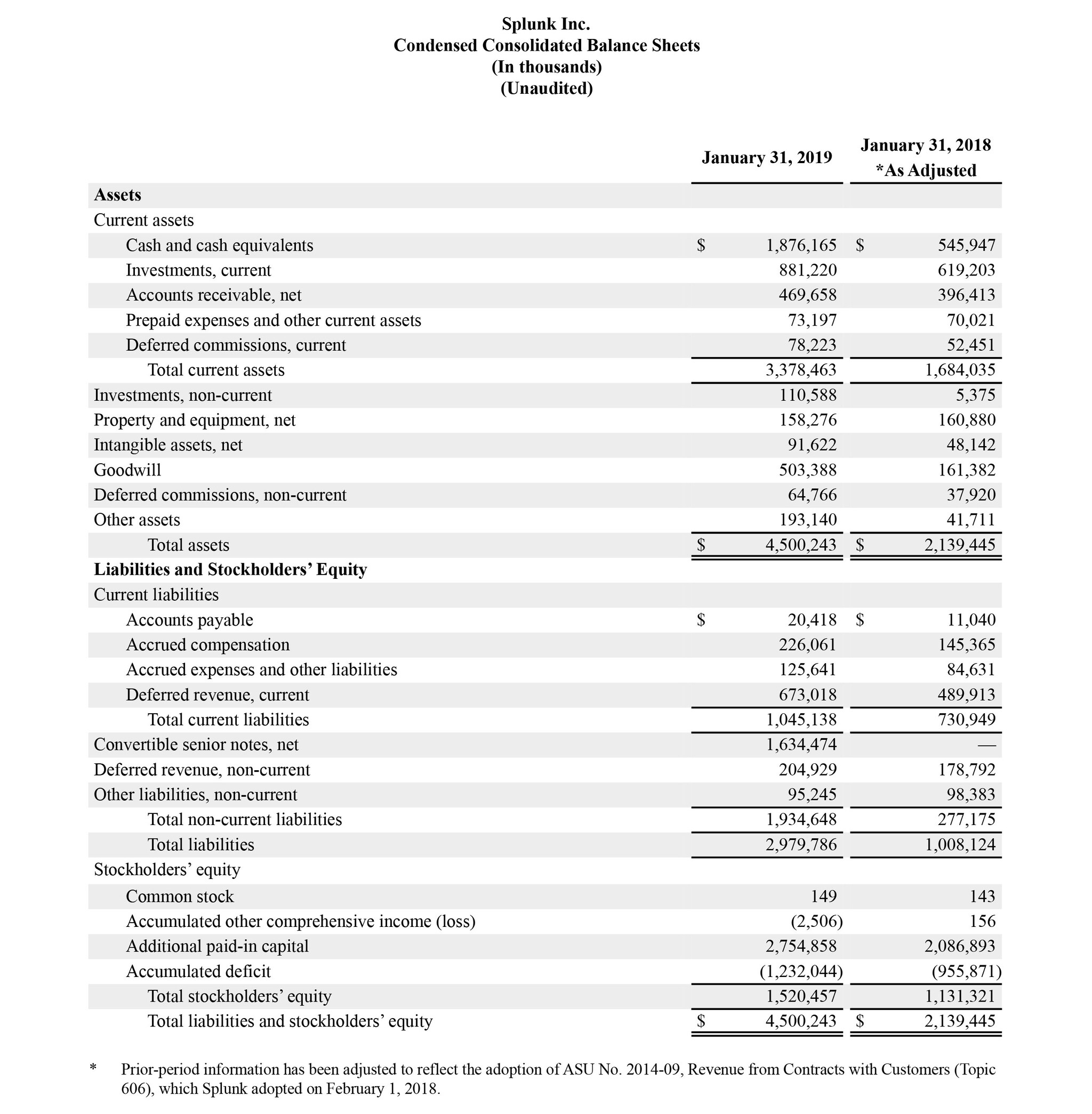

Splunk Inc Announces Fiscal Fourth Quarter And Full Year 2019 Financial Results Splunk

Disposing Of Irc 197 Intangibles It S All Or Nothing

Complex Deals Class 10 M A Tax Issues And Acquisition Accounting Ppt Download